Hard Money Lenders Rochester: What You Need to Know

- Published on

-

Joseph Gordon EditorClose

Joseph Gordon Editor

Joseph Gordon EditorClose

Joseph Gordon EditorJoseph Gordon is an Editor with HomeLight. He has several years of experience reporting on the commercial real estate and insurance industries.

If you’re a real estate investor in Rochester, you know the local market can move quickly, and having access to flexible financing is essential. Whether you’re looking to flip homes in the South Wedge or purchase rental properties near Park Avenue, hard money lenders could offer the short-term funding you need to secure a deal fast.

Hard money loans differ from traditional financing in that they prioritize the property’s value over the borrower’s credit. These loans can be a good option for investors who need quick access to cash, especially in a competitive market like Rochester’s.

If you’re exploring options for your next project, understanding the benefits and potential costs of working with a hard money lender can help you decide whether it’s the right move for you. Hard money loan options can be a key strategy for some investors.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

Editor’s note: This post is for educational purposes and is not intended to be construed as financial advice. HomeLight always encourages you to consult your own advisor.

What is a hard money lender?

Hard money lenders provide short-term loans primarily to real estate investors, including buyers of rental properties and house flippers. Instead of focusing on the borrower’s credit score, these lenders assess the property’s potential value after renovations, known as the after-repair value (ARV), to determine the loan amount.

Interest rates for hard money loans are typically higher than traditional loans, often ranging between 8% and 15%, with additional fees such as origination costs and points. If a borrower cannot repay the loan, the lender has the right to take ownership of the property, using it as collateral. This makes hard money loans a high-risk, high-reward financing option for both the lender and the borrower.

How does a hard money loan work?

Hard money loans in Rochester work differently from traditional mortgages, offering unique advantages and challenges for investors. Here’s a breakdown of how these loans function and what you can expect:

- Short-term loan: Hard money loans are short-term, typically lasting 6 to 24 months, unlike a traditional 30-year mortgage. They’re designed to bridge a financial gap for investors.

- Faster funding option: While traditional loans can take 30 to 50 days to process, hard money lenders can often provide funding within days, making them ideal for quick real estate deals.

- Less focus on creditworthiness: Hard money lenders pay less attention to a borrower’s credit score. Instead, they assess the potential of the property itself.

- More focus on property value: These loans rely heavily on the loan-to-value ratio and the property’s future after-repair value (ARV) to determine loan amounts.

- Not traditional lenders: Hard money lenders are private individuals or companies, not banks or government-backed institutions, which allows for more flexible terms.

- Loan denial option: Unlike traditional lenders, hard money lenders can deny a loan based on the property’s risk or potential, even if a borrower’s creditworthiness is solid.

- Higher interest rates: Expect interest rates significantly higher than traditional loans, often ranging between 8% and 15%, compared to conventional rates for a 30-year mortgage.

- Might require larger down payments: Hard money loans typically require a down payment of 20%–30% or more to secure the property.

- More flexibility: Lenders may be more flexible with loan terms and repayment schedules compared to traditional mortgage options.

- Potential for interest-only payments: In some cases, borrowers may only be required to make interest payments until the end of the loan term, with the balance paid at the close of the loan.

What are hard money loans used for?

Hard money loans can be a helpful financing option in real estate situations, particularly when traditional financing is difficult to secure. Here’s how hard money loans can help in different scenarios, from flipping homes to avoiding foreclosure.

- Flipping a house

For flipping homes, hard money loans provide fast access to capital, enabling investors to purchase properties and fund renovations. The short-term nature of these loans aligns with the quick turnaround required to buy, rehab, and sell a property for profit. - Buying an investment rental property

When purchasing rental properties, a hard money loan allows investors to secure a property quickly, even in competitive markets. This is especially useful when a property needs significant repairs, making it ineligible for traditional mortgage financing. - Purchasing commercial real estate

Investors looking to acquire commercial properties may use hard money loans when traditional lenders are slow or unwilling to finance the deal. Hard money loans provide flexibility, allowing investors to act quickly and leverage the property’s value to secure financing. - Borrowers who can’t qualify for traditional loans

For individuals with lower credit scores or other financial challenges, hard money loans offer a way to obtain financing when banks turn them away. Since the loan is based on the property’s value, it bypasses typical lending hurdles. - Homeowners facing foreclosure

Hard money loans can be a lifeline for homeowners in pre-foreclosure property sale. These loans provide quick funds, allowing homeowners to pay off their debts or leverage their equity to avoid losing their property.

How much do hard money loans cost?

Hard money loans generally cost more than traditional loans due to the higher risk for lenders and the convenience of quick, flexible funding. Typical costs include:

- Interest rates: 8% to 15% or higher, based on risk assessment.

- Origination fees: 1% to 5% of the loan amount.

- Closing costs: Legal, appraisal, and administrative fees.

- Points: A percentage of the loan amount charged upfront.

Online calculators can help estimate these costs.

Alternatives to working with hard money lenders

If you’re exploring alternatives to hard money loans, here are several financing options to consider:

Take out a second mortgage: If you have substantial equity in your home, a home equity loan or home equity line of credit (HELOC) could provide funds at a lower interest rate than a hard money loan.

Cash-out refinance: A cash-out refinance lets you pull equity from an existing property to finance your next project, often offering better terms than a hard money loan.

Borrow from family or friends: Personal loans from family or friends can be a more flexible and affordable option, with the potential for lower or no interest rates.

Use a government-backed loan program: Programs like FHA, VA, or USDA loans may offer more affordable financing options with lower down payments and interest rates.

Peer-to-peer loan: Peer-to-peer lending platforms allow you to borrow directly from individual investors, often with different terms and conditions than a traditional hard money loan.

Specialized loan programs: Some lenders offer loans specifically designed for fixer-uppers or investment properties, which can be an alternative if you’re already holding a hard money loan and want to refinance.

Request a seller financing option: In certain cases, sellers may agree to finance the purchase themselves, which could lead to fewer closing costs and less strict eligibility requirements.

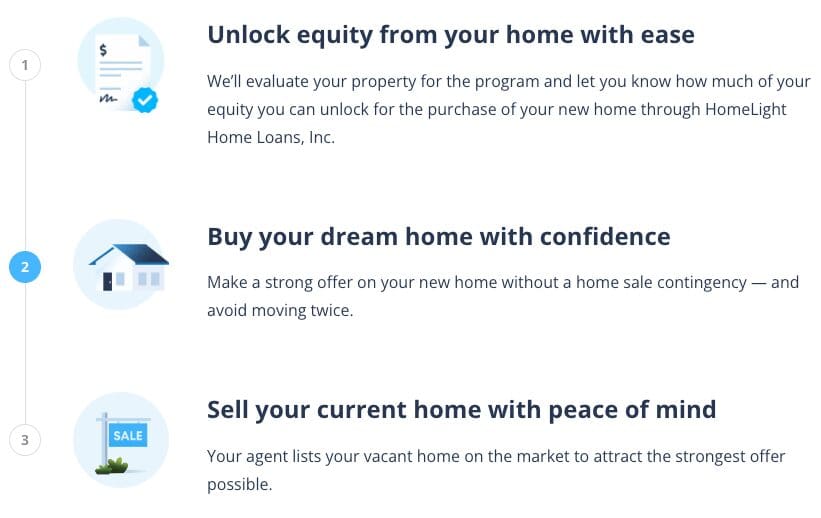

How to buy before you sell

HomeLight’s Buy Before You Sell program allows homeowners to buy a new home before selling your current one, easing the stress of coordinating timelines between selling and buying. Through this program, HomeLight purchases your new home on your behalf with a guaranteed offer, allowing you to move in right away. Once you’ve moved, HomeLight helps you sell your old home for top dollar, maximizing your proceeds.

The Buy Before You Sell (BBYS) program allows you to leverage the equity in your existing home to make a stronger, non-contingent offer on a new property. If your home qualifies, you can get your equity unlock amount approved in 24 hours or less, with no cost or commitment required. Once approved, you can confidently purchase your next home and then sell your current one vacant, avoiding the hassle of moving twice.

Here’s how HomeLight Buy Before You Sell works:

Although there’s a flat fee of 2.4% of your current home’s sold price, the potential savings you could see in other areas might outweigh the cost. For example, you might save on moving expenses, temporary housing, and even the final purchase price of your new home. On top of that, HomeLight’s BBYS fees are typically much lower than the interest rates on bridge loans, which currently range from 9.5% to 12%.

3 top hard money lenders in Rochester

Traditional lenders might not be the solution for every real estate investment. If you’re looking to move quickly and capitalize on an opportunity, explore the hard money lending options available in Rochester.

Tompkins Lending

Tompkins Lending is a private lending firm specializing in offering flexible financing solutions to real estate investors. The company provides a range of loan products, including hard money loans for fix-and-flip projects, rental property investments, and commercial real estate deals.

Lending clientele: Residential and commercial real estate investors

Loan criteria: LTV up to 95% of ARV

Tompkins Lending has a strong reputation for its customer service and the speed of its loan processing. The company has a 5.0-star rating on Google. Reviews note the firm’s ability to close deals quickly and its commitment to meeting the unique needs of each investor.

585-271-2400

Webster Capital

Webster Capital is a private commercial real estate lender specializing in quick, reliable financing solutions for investors and developers. They offer various loan products, including fix-and-flip, new construction, and bridge loans, with a streamlined process for fast approvals and closings.

Lending clientele: Residential and commercial real estate investors

Loan criteria: LTV up to 85% of ARV

Webster Capital has a 5.0-star rating on Google based on numerous positive reviews. Reviews commend the company for its quick and efficient process, transparency, and personalized service.

585-451-2583

New Silver

New Silver provides real estate investment loans in 39 states, including Massachusetts. Founded in 2018, the company offers fix-and-flip loans, rental property loans, and ground-up construction loans. They specialize in financing non-owner-occupied properties in urban or suburban areas with 1–50 units. Closing times typically range from five to 10 days, though it may take longer depending on the property’s location.

Lending clientele: Residential real estate investors

Loan criteria: Varies by loan program

New Silver holds a 3.9-star rating on Google. Reviews praise the company for its quick closings, prompt communication, and high loan-to-value ratios. However, some negative reviews highlight misleading information on their website and an unprofessional operator.

855-844-5626

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Should I partner with a hard money lender in Rochester?

Determining if a hard money loan is the right choice depends on your specific needs and timeline. These loans are tailored for real estate investors who require fast funding to complete projects like flipping homes, purchasing rental properties, or investing in commercial real estate.

With flexible terms and a focus on property value, hard money loans can help you move quickly in Rochester’s competitive real estate market. However, they come with higher interest rates and shorter repayment periods, making them better suited for short-term investments.

If you’re a homeowner in Rochester looking to unlock your home’s equity but you’re not in the real estate investment business, HomeLight has an alternative. The Buy Before You Sell program lets you purchase a new home before selling your current one, making the transition smoother. It’s a great way to leverage your equity without the pressure of lining up selling and buying at the same time. Learn more about HomeLight’s offerings at HomeLight.

Header Image Source: (photoquest7/DepositPhotos)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.