Hard Money Lenders San Antonio: Flexible Loan Options

- Published on

- 11 min read

-

Kelsey Morrison Former HomeLight EditorClose

Kelsey Morrison Former HomeLight Editor

Kelsey Morrison Former HomeLight EditorClose

Kelsey Morrison Former HomeLight EditorKelsey Morrison worked as an editor for HomeLight's Resource Centers. She has seven years of editorial experience in the real estate and lifestyle spaces. She previously worked as a commerce editor for World of Good Brands (eHow.com and Cuteness.com) and as an associate editor for Livabl.com. Kelsey holds a bachelor’s degree in Journalism from Concordia University in Montreal, Quebec, and lives in a small mountain town in Southern California.

Looking to fund your next real estate project in San Antonio with a hard money loan? Whether you’re scoping out a charming fixer-upper in Woodlawn or planning to purchase a commercial property downtown, hard money lenders in San Antonio offer the speed and flexibility you need. Hard money loans serve as an alternative to traditional financing, and are especially useful for those with tight project timelines, limited capital, or credit challenges.

For homeowners not involved in real estate investing but needing to bridge the gap between buying and selling, we’ll explore some practical alternatives to leverage your home’s equity. This guide will walk you through the essentials of hard money lending in San Antonio, helping you determine if this financing option aligns with your real estate investment or home-buying goals.

Start Making Offers Without Waiting to Sell Your Home

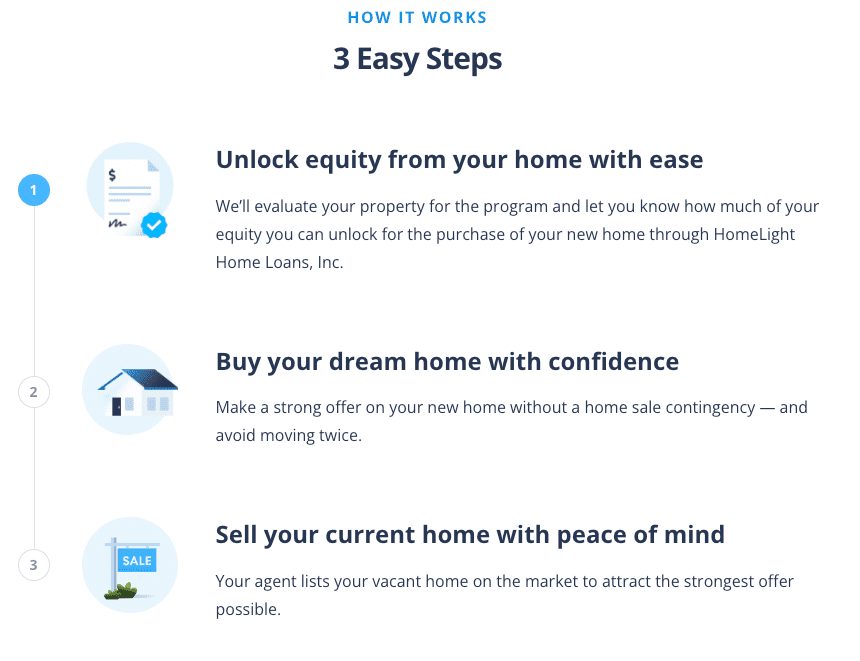

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

What is a hard money lender?

A hard money lender is a private individual or company that offers short-term loans secured by real estate. Unlike traditional lenders, who focus heavily on the borrower’s creditworthiness and income, hard money lenders in San Antonio prioritize the value of the property being used as collateral. These lenders cater to real estate investors, including house flippers and those purchasing rental properties, who need quick access to funds and flexible terms.

Hard money lenders use after-repair value (ARV) — the estimated value of a property after all renovations and repairs are completed — to determine the loan amount they are willing to offer. They typically lend a percentage of the ARV to ensure the investment’s profitability and security.

Hard money loans generally have higher interest rates, ranging from 8% to 15% or more, and shorter repayment periods, usually between 6 to 24 months. Additional costs can include origination fees, closing costs, and points. If a borrower fails to repay a hard money loan, the lender can seize the asset to recover their investment.

How does a hard money loan work?

If you’re a real estate investor in San Antonio seeking a fast and flexible financing solution, hard money loans might be the perfect fit. Here’s a quick overview of how hard money loans work:

- Short-term loan: These loans usually have a repayment period of 6–24 months, unlike the 15- or 30-year terms of conventional mortgages. Some lenders might extend the term up to 36 months if necessary.

- Faster funding option: When you need to close a deal quickly, hard money loans can be approved within days, compared to the 30 to 50 days typical for a mortgage loan.

- Less focus on creditworthiness: Approval relies less on your credit score or income history and more on the property’s value.

- More focus on property value: These loans are based on the loan-to-value ratio of the property, requiring collateral such as a home.

- Not traditional lenders: Hard money loans are usually provided by individual investors or private lending companies, not traditional banks.

- Loan denial option: These loans are often used by those with poor credit who have been denied a mortgage but have significant home equity.

- Higher interest rates: Due to the higher risk, hard money loans have higher interest rates than traditional mortgages.

- Might require larger down payments: Borrowers may need to provide a larger down payment, sometimes up to 20%–30%, depending on the property’s value and loan specifics.

- More flexibility: With less government regulation, hard money lenders in San Antonio can set flexible credit scores and debt-to-income criteria, and loans can help homeowners avoid pre-foreclosure property sale.

- Potential for interest-only payments: Unlike traditional mortgages, hard money loans may allow for interest-only or deferred payments at first.

What are hard money loans used for?

Hard money loans serve specific needs within the San Antonio real estate market. These loans are often sought by investors and homeowners who require quick funding or face challenges with traditional bank loans. Here’s a look at common uses for hard money loans:

Flipping a house: San Antonio investors focusing on flipping homes can benefit from hard money loans due to their speedy approval and funding process. These loans allow flippers to quickly purchase and renovate properties, allowing them to sell for a profit in a short period.

Buying an investment rental property: For those eyeing rental properties, hard money loans offer a fast way to acquire properties that need immediate attention. The quick access to funds helps investors complete necessary renovations and start generating rental income sooner.

Purchasing commercial real estate: In the commercial real estate sector, timing is often critical. Hard money loans provide the flexibility and quick funding needed to secure valuable investments in a timely manner, making them ideal for commercial property purchases.

Borrowers who can’t qualify for traditional loans: Individuals with significant home equity but poor credit histories often turn to hard money lenders. These loans focus more on the value of the property rather than the borrower’s credit score, providing an alternative route to financing.

Homeowners facing foreclosure: Hard money loans can be a lifeline for homeowners at risk of foreclosure. These loans offer a way to refinance debts or buy additional time to sell the property, helping to avoid the negative impact of foreclosure on credit records.

How much do hard money loans cost?

The cost of hard money loans is typically higher due to the increased risk and convenience of fast, flexible funding. Here are some typical costs associated with hard money loans:

- Interest rates: These can range from 8% to 15% or higher, depending on the lender’s risk assessment.

- Origination fees: Lenders may charge 1% to 5% of the total loan amount.

- Closing costs: Additional fees at closing can include legal fees, appraisal fees, and other administrative costs.

- Points: Lenders might charge points (a percentage of the loan amount) upfront, adding to the initial cost.

Online calculators can help estimate these costs accurately.

Alternatives to working with hard money lenders

If you’re not an investor, but rather a homeowner looking to tap into your current home’s equity, you may want to consider the following options:

Take out a second mortgage: Utilize your home’s equity by obtaining a home equity loan or a home equity line of credit (HELOC), which generally offer lower interest rates compared to hard money loans.

Cash-out refinance: This strategy allows you to refinance your current mortgage, extracting cash from the home’s equity to fund new investments, often with more favorable interest rates.

Borrow from family or friends: Personal loans from family or friends can provide flexible repayment terms and potentially lower or no interest rates, making them a cost-effective alternative.

Use a government-backed loan program: Programs from the FHA, VA, or USDA can help you purchase homes with smaller down payments and reduced interest rates, easing the financing process.

Peer-to-peer loans: Borrow through peer-to-peer lending platforms, where individual investors provide funds. These loans can offer unique terms that are different from traditional and hard money loans.

Specialized loan programs: Look into specialized financing options designed for fixer-uppers or refinancing existing investment properties, which might offer better terms than a hard money loan.

Request a seller financing option: Some sellers may offer to finance the purchase themselves, potentially lowering closing costs and easing qualification criteria.

How to buy before you sell

Imagine finding your dream home in San Antonio just as it hits the market, perhaps a Craftsman-style house in Southtown or a newly-built townhouse near the Pearl District. HomeLight’s Buy Before You Sell (BBYS) program is designed to help homeowners like you secure a new home before selling your current one, making the transition smoother and less stressful.

The Buy Before You Sell program allows you to use the equity in your current home to make a compelling, non-contingent offer on a new property. If your home qualifies, you can get an equity unlock amount approved within 24 hours, with no initial cost or commitment. This enables you to buy your new home first and sell your old one after, avoiding the inconvenience of moving twice.

Here’s how HomeLight Buy Before You Sell works:

The program charges a flat fee of 2.4% of your home’s selling price. However, the potential savings from avoiding temporary housing, moving costs, and possibly securing a better deal on your new home can make this fee worthwhile. Additionally, HomeLight’s BBYS fees are generally lower than the interest rates on bridge loans, which typically range from 9.5% to 12%.

3 top hard money lenders in San Antonio

Traditional lenders may not always suit every real estate investment. If you need to move quickly on a promising opportunity, consider these top-rated hard money lenders in San Antonio.

Noble Mortgage & Investments

Noble Mortgage & Investments provides commercial and residential hard money loans all over Texas. Founded in 2003, the company has several different loan products including fix-and-flip, fix-to-rent, new construction, and commercial. For San Antonio investors who are buying and improving distressed properties, Noble Mortgage & Investments will fund up to 100% of the purchase price, repairs and closing costs. Borrowers can get a free pre-approval letter within two business days, and loans are typically funded within seven to 10 business days.

Lending clientele: Residential and commercial real estate investors, plus homeowners

Loan criteria: Up tp 75% LTV (fix-to-rent), up to 75% ARV (fix-and-flip), up to 70% LTV (commercial), up to 70% LTV (new construction)

Noble Mortgage & Investments boasts a 5-star rating on Google based on well over 300 reviews. Customers appreciate their fast service, competitive terms and rates, and frequent communication. “Working as an escrow officer for a title company, I get to see all sorts of lenders, but Noble Mortgage? They’re in a league of their own. They are amazing at what they do, always going the extra mile for their clients,” reads a recent review.

832-219-7745

Longhorn Investments

Established in 2008, Longhorn Investments is a Texas-based direct private lender specializing in hard money loans for real estate investors. They offer a hard money lending product to San Antonio investors looking to flip houses or rehab rental properties. Residential hard money loans apply to single-family homes and two- to four-unit townhomes only; Longhorn Investments will not consider condominiums or manufactured homes. Loans typically close in just three to five business days, and are based on the after repair value (ARV) of the property.

Lending clientele: Residential and commercial real estate investors

Loan criteria: Up to 75% of the ARV (rentals), up to 70% of the ARV (flips)

Boasting a 5-star rating on Google with over 200 reviews, Longhorn Investments is commended for its smooth loan process, fast communication, and supportive staff. “Great choice for my first flip,” wrote one client. “They answered all of my questions whenever I needed guidance. After speaking with other lenders, I quickly realized that I made the right decision to use Longhorn.”

877-420-7346

Little City Investments

Based in nearby Austin, Little City Investments was founded in 2006 by a real estate broker with a flipping and development background. They are direct lenders who fund a variety of loans for residential and commercial real estate investors. The company operates in the San Antonio, Austin, Houston, and Dallas areas. Loans can close in around three to five days and are are primarily based on real estate value, not credit or income.

Lending clientele: Residential and commercial real estate investors

Loan criteria: Up to 75% LTV

Little City Investments has a 5-star rating on Google based on a limited number of reviews. Customers highlight their quick closing times, responsiveness, and honesty. “They did a great job of not only managing expectations but also closing quickly,” wrote one reviewer. “I would highly recommend them and I plan on working with them together in the future.”

512-577-6049

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Should I partner with a hard money lender in San Antonio?

The decision to use a hard money lender in San Antonio should be based on your specific circumstances and real estate investment goals. Hard money loans are particularly well-suited for real estate investors needing quick access to funds, especially for projects with short timelines or when traditional financing just isn’t feasible.

If you’re prepared to handle higher costs and shorter repayment terms for the sake of fast, flexible funding, connecting with a hard money lender in San Antonio might be the right move for your next investment opportunity.

For homeowners looking to tap into their home’s equity without dealing with high interest rates, HomeLight’s Buy Before You Sell program is a great option. Rather than facing steep interest rates, you’ll pay a small flat fee and enjoy the benefits of a competitive offer and an easier moving process.

As with any major financial decision, it’s important to consider your long-term strategy and consult with a financial advisor to make sure it aligns with your overall investment goals. If you’re looking to connect with real estate agents in San Antonio who can introduce you to trusted hard money lenders, HomeLight can help you find top professionals in your area.

Header Image Source: (f11photo / Depositphotos)

- "What is ARV and how is it calculated?," Rehab Financial Group (June 2023)

- "What Is Loan-to-Value and Why Does it Matter?," U.S. News, Ben Luthi & Rebecca Safier (March 2024)

- "Why Do Hard Money Lenders Require A Down Payment?," RCN Capital (April 2024)

- "A Comprehensive Guide to Common Terms Used in Hard Money Lending," LinkedIn, Joseph Walker (September 2023)

- "What Are The Costs Involved In A Hard Money Loan?," NorthWest Private Lending (March 2024)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.