Hard Money Lenders Washington, DC: Alternative Financing

- Published on

- 10 min read

-

Joseph Gordon EditorClose

Joseph Gordon Editor

Joseph Gordon EditorClose

Joseph Gordon EditorJoseph Gordon is an Editor with HomeLight. He has several years of experience reporting on the commercial real estate and insurance industries.

Timing can be everything in the fast-paced real estate market of Washington, D.C. For buyers and investors looking to capitalize on an investment quickly, traditional loans might not cut it. This is where hard money loans come into play. They offer a different route to securing the funds needed for various real estate transactions in the nation’s capital. Whether you’re eyeing a rowhouse in Capitol Hill or considering a fixer-upper in Shaw, hard money loans can provide the speed and flexibility you need.

Hard money loans aren’t your everyday mortgages; they cater to those who need financing fast and aren’t put off by higher interest rates. If you’re in the D.C. market and want to learn how these loans work, when they’re most useful, and what they might cost, this guide will walk you through the essentials to help you make an informed decision.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

Editor’s note: This post is for educational purposes and is not intended to be construed as financial advice. HomeLight always encourages you to consult your own advisor.

What is a hard money lender?

A hard money lender is a private entity or individual that provides short-term loans secured by real estate. Unlike banks that prioritize a borrower’s financial history, these lenders place more importance on the property’s value. This makes hard money loans appealing to house flippers and rental property investors needing swift financing.

Hard money lenders use the after-repair value (ARV), which is the projected worth of a property after renovations, to decide how much to lend. They typically offer a percentage of this ARV to minimize their risk.

These loans come with higher interest rates, usually between 8% and 15%, along with fees like origination costs. If the borrower defaults, the lender can take ownership of the property to recover the funds.

How does a hard money loan work?

If you’re a real estate investor in Washington, D.C., needing fast and flexible financing, hard money loans might be the right fit. Here’s a breakdown of how these loans work and what you can expect:

- Short-term loan: These loans typically have a repayment period of 6–24 months, much shorter than a 30-year conventional mortgage. In some cases, terms can extend up to 36 months.

- Faster funding option: Unlike traditional loans that can take 30 to 50 days to process, hard money loans can be approved in just a few days, allowing investors to move quickly.

- Less focus on creditworthiness: Hard money lenders place less emphasis on your credit score and financial history, focusing more on the property itself.

- More focus on property value: The loan amount is primarily based on the loan-to-value ratio of the property, making the property’s value crucial for approval.

- Not traditional lenders: These loans come from private investors or companies rather than banks, offering more tailored terms to meet individual needs.

- Loan denial option: Hard money loans are often used by individuals with poor credit who have been denied traditional mortgages but have significant home equity.

- Higher interest rates: Due to the increased risk, hard money loans have higher interest rates than conventional mortgages.

- Might require larger down payments: Borrowers may need a larger down payment, often ranging from 20%–30% of the property’s value.

- More flexibility: With less regulation than traditional lenders, hard money lenders can be more flexible with debt-to-income criteria and credit scores, potentially offering solutions to avoid foreclosure.

- Potential for interest-only payments: Some hard money loans allow for interest-only or deferred payments at the beginning of the loan term, easing the initial cash flow.

What are hard money loans used for?

Hard money loans fulfill a unique niche in the Washington, D.C., real estate market, providing funding options for various situations. Here’s how they can be utilized:

Flipping a house

Investors in flipping homes use hard money loans for their quick funding capabilities. These loans enable them to purchase and renovate properties, allowing for fast turnaround and profit.

Buying an investment rental property

Hard money loans are perfect for snapping up rental properties that need immediate work. With quick access to funds, landlords can renovate and rent out these properties sooner than with traditional financing.

Purchasing commercial real estate

In commercial real estate, timing can make or break a deal. Hard money loans offer the speed needed to secure investments without the delays typical of conventional loans.

Borrowers who can’t qualify for traditional loans

Individuals with significant home equity but poor credit often turn to hard money loans. These loans emphasize the property’s value over credit history, providing an alternative financing route.

Homeowners facing foreclosure

For those at risk of foreclosure, hard money loans can serve as a temporary solution. They offer refinancing options or extra time to sell the property, potentially helping homeowners avoid foreclosure.

How much do hard money loans cost?

Hard money loans generally cost more than traditional loans due to the higher risk for lenders and the convenience of quick, flexible funding. Typical costs include:

- Interest rates: 8% to 15% or higher, based on risk assessment.

- Origination fees: 1% to 5% of the loan amount.

- Closing costs: Legal, appraisal, and administrative fees.

- Points: A percentage of the loan amount charged upfront.

Online calculators can help estimate these costs.

Alternatives to working with hard money lenders

Exploring alternatives to hard money loans? Here are some options to consider:

- Take out a second mortgage: Use a home equity loan or HELOC to borrow against your home’s equity. These typically offer lower interest rates than hard money loans.

- Cash-out refinance: Refinance your mortgage to access your home’s equity in cash. A cash-out refinance can often provide lower interest rates compared to hard money options.

- Borrow from family or friends: Personal loans from family or friends can offer flexible terms and potentially lower or no interest, making them a more affordable choice.

- Use a government-backed loan program: Programs from the FHA, VA, or USDA can help with lower down payments and interest rates, providing government-supported assistance.

- Peer-to-peer loan: Obtain a loan from individual investors through platforms like MeridianLink or Funding Circle. These loans can offer terms that differ from traditional hard money loans.

- Specialized loan programs: If dealing with a fixer-upper or seeking to refinance an investment property, look into specialized loan programs that might offer more suitable terms.

- Request a seller financing option: Some sellers may offer to finance the purchase themselves, leading to lower closing costs and more flexible eligibility requirements.

How to buy before you sell

If you’re looking to buy a new home before selling your current one, HomeLight offers a convenient solution. The Buy Before You Sell program lets you leverage the equity in your current home to make a competitive, non-contingent offer on a new property. This way, you can secure your next home without the pressure of selling first.

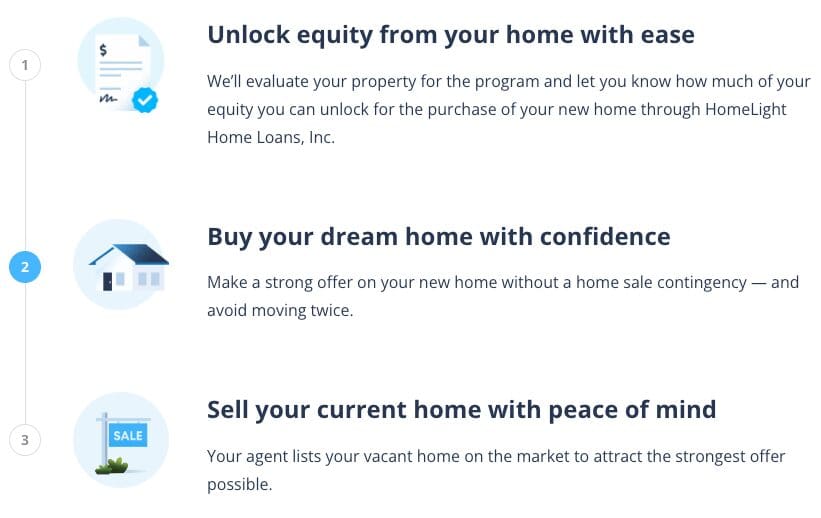

Here’s how it works: HomeLight helps you unlock your home’s equity, getting approval within 24 hours at no initial cost or commitment. Once approved, you can purchase your new home with confidence. After you move, you can sell your previous home vacant, letting you avoid the hassle of multiple moves:

Here’s how HomeLight Buy Before You Sell works:

The program charges a flat fee of 2.4% of your home’s final sale price. However, savings in other areas might offset this cost, such as avoiding temporary housing or moving expenses. Plus, HomeLight’s fees are generally lower than bridge loan interest rates, which range from 9.5% to 12%.

3 top hard money lenders in Washington, DC

Traditional lenders might not be the solution for every real estate investment. If you’re looking to move quickly and capitalize on an opportunity, explore the hard money lending options available in Washington, DC.

Great Jones Capital

Great Jones Capital specializes in private real estate lending. It provides customized financial solutions for various real estate investments, offering bridge loans, fix-and-flip loans, and construction loans.

Lending clientele: Residential, construction, and commercial real estate investors

Loan criteria: LTV up to 80% of ARV

Great Jones Capital has earned a 3.4-star rating on Google. Clients appreciate the firm’s efficiency and the team’s expertise.

202-810-5273

RevitaLending

RevitaLending is a private lending firm that offers fix-and-flip loans, bridge loans, and rental property loans. It offers quick closings and tailored loan structures to meet each investor’s unique needs.

Lending clientele: Residential and commercial real estate investors

Loan criteria: RevitaLending’s specific LTV (Loan-to-Value) ratio isn’t mentioned directly on its website. You may want to contact them directly or check with a loan officer for precise details on its loan criteria, including the maximum LTV it offers.

RevitaLending has earned a 3.0-star rating on Google. Clients often commend the company’s efficiency and personalized service.

202-595-5472

Washington Capital Partners

Washington Capital Partners provides hard money loans to investors, as well as offering fix-and-flip, rental, new construction, and bridge loans. It can often close within 7-10 days.

Lending clientele: Residential and commercial real estate investors

Loan criteria: LTV up to 70% of ARV

Washington Capital Partners has earned a 4.5-star rating on Google. Clients often highlight the company’s efficiency, professionalism, and excellent customer service.

703-348-0549

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Should I partner with a hard money lender in Washington, DC?

Choosing a hard money loan in Washington, D.C., depends on your needs and investment goals. These loans are ideal for real estate investors who require fast, flexible funding for projects like flipping houses or securing rental properties.

If you can handle higher interest rates and shorter repayment periods for the benefit of quick financing, a hard money lender might be the right choice for your D.C. investment ventures.

For homeowners aiming to leverage their home’s equity to purchase a new property, HomeLight’s Buy Before You Sell program can be a more fitting option. This alternative lets you avoid the steep interest rates of hard money loans, offering a simpler and more affordable way to make a strong offer on your next home.

Before deciding, it’s important to consider your long-term financial goals. Consulting a financial advisor can help ensure that your choice aligns with your overall strategy. For more assistance, HomeLight can connect you with experienced professionals and programs tailored to your needs.

Header Image Source: (Ian McDonald/Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.