What Is a Home Equity Sharing Agreement?

- Published on

- 15 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

You have equity in your home and need cash. But a traditional home equity loan won’t work for you because you can’t afford more monthly payments, or your credit score won’t allow it. A home equity sharing agreement might be the solution you need.

This unique financing option lets you unlock money from your home’s equity without the burden of monthly loan payments. By partnering with an investor or equity sharing company, you can get a lump-sum cash advance in exchange for a share of your home’s future appreciation.

How Much Is Your Home Worth Now?

Home values have rapidly increased in recent years. How much is your current home worth now? Get a ballpark estimate from HomeLight’s free Home Value Estimator.

In this guide, we’ll explain how a home equity sharing agreement works and how it can benefit you, and provide information to help you decide whether this option is right for you. We’ll also share tips and insights from a top home equity sharing expert.

What is a home equity sharing agreement?

“A home equity sharing agreement, also known as a home equity agreement (HEA), is a no-loan option for homeowners to access the equity they’ve built in their homes,” explains Michael Micheletti, chief marketing officer at Unlock, a leading home equity sharing company. “Homeowners receive cash up front (the amount varies by provider) in exchange for a portion of their home’s future value.”

With an HEA, a homeowner sells a slice of their home’s future appreciation to an investor in exchange for upfront funds they can use immediately.

“Because a home equity agreement or home equity sharing doesn’t involve a loan, there are no interest charges or monthly payments for homeowners,” Micheletti says. Instead, the homeowner agrees to share a percentage of the property’s future value when it’s sold, refinanced, or after a specified period.

This arrangement can be especially beneficial to homeowners with less-than-perfect credit scores.

How does home equity sharing work?

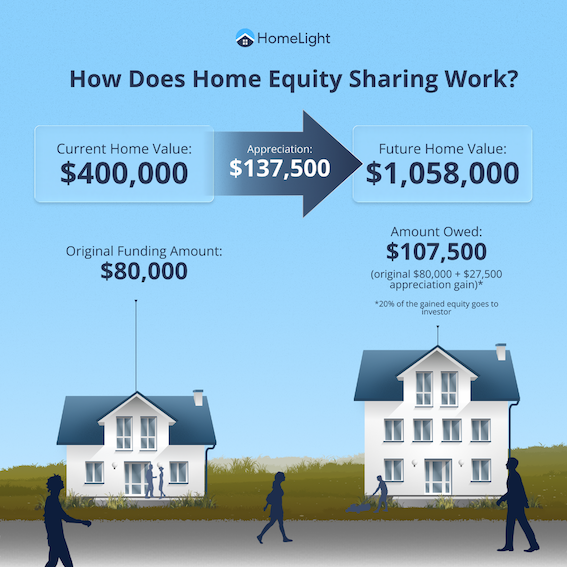

Let’s look at an example of what a home equity sharing agreement might look like. In this scenario, we’ll use a $400,000 property value. This could be how much your paid-off home is worth or how much equity stake you own in the house.

If an equity sharing company buys a 20% stake in your home equity and your house is worth $400,000, the investor group would give you an $80,000 lump sum.

- Your home’s current value: $400,000

- Amount of cash you need: $80,000

- Investment company’s stake: 20%

- Home equity sharing contract term: 10 years

- Home’s annual appreciation rate: 3%

At the end of 10 years, the house appreciates to about $537,500. The homeowner will need to pay back the original investment ($80,000) plus the investor’s 20% stake in the home’s $137,500 appreciation amount ($27,500). In this case, the payback amount would be about $107,500.

“During the term of the HEA, homeowners are responsible for continued, regular payment of existing obligations on their property, including mortgage payments, homeowners’ association fees, and all local and/or state property taxes.”

“They are also responsible for the care and upkeep of the property, including all repairs, maintenance, and other associated costs,” Micheletti says.

He adds that some home equity agreement companies, like Unlock, provide adjustments for home improvements made during the term of the agreement. “So homeowners keep the value created by those improvements.”

What if your home decreases in value?

With a home equity sharing agreement, the company shares in both the appreciation and depreciation of your property.

If your home’s value decreases, the amount you owe the company will also decrease. Let’s take the example above. If your home’s value drops from $400,000 to $380,000 and the company has a 20% equity share, it would receive $60,000 rather than the original $80,000.

Our table below illustrates the breakdown of the home equity sharing scenario, what happens if the home appreciates and depreciates in value.

| If your house appreciates | If your house depreciates | |

| Starting home value | $400,000 | $400,000 |

| Home value at repayment | $537,500 | $380,000 |

| Total increase or decrease | $137,500 | -$20,000 |

| Shared equity percentage | 20% (for gain of $27,500) | N/A (for loss of $20,000) |

| Original funding amount | $80,000 | $80,000 |

| Amount you owe the investor | $107,500 | $60,000 |

Repayment obligations vary: The amount you owe at the end of your home equity sharing agreement will depend on the terms of your contract. Repayment requirements vary. Our example scenario shows a common, simplified model. Your final obligation will be based on a percentage of your home’s value at the end of the contract term.

What’s the home equity sharing agreement process?

Here’s a look at the steps you might expect in a home equity sharing process:

- Vet home equity sharing companies: Begin by researching reputable home equity sharing companies. Look for reviews, check their track record, and ensure they have transparent terms and conditions.

- Request a pre-qualification estimate: Once you’ve shortlisted a few companies, request a pre-qualification estimate to understand how much equity you can access based on your home’s value and other factors.

- Get a home appraisal: Your home will be appraised to determine its current market value. This is a crucial step in setting the terms of the agreement.

- Receive your cash advance: After the appraisal and finalizing the agreement, you’ll receive a lump sum cash payment from the investor. This provides you with the funds you need without additional monthly debt.

- Worry not about monthly payments: One significant advantage of a home equity sharing agreement is that you don’t have to make monthly payments. The investor’s return is tied to the future value of your home.

- When the term ends, pay back the equity value: At the end of the agreement, when you sell or refinance your home or at the end of a set number of years, you’ll pay back the investor based on the agreed-upon terms, which typically include a percentage of your home’s appreciated value or selling price.

“Home equity sharing companies receive their share of the home’s value when a homeowner sells the property or in a lump sum at the end of their home equity agreement, which can vary between 10 to 30 years depending on the HEA provider,” Micheletti explains.

If you’re accessing cash from equity to help you buy before you sell, check out HomeLight’s innovative Buy Before You Sell program, which offers a streamlined, simplified, and more certain process. Watch this short video to learn more.

Are there different types of equity sharing agreements?

“Every company structures its agreements slightly differently,” Micheletti says. “Unlock and many of the companies operating in this space provide investments based on sharing a portion of a home’s future value.”

The agreement you enter into will be distinguished by how the investor’s return is calculated:

- Share of appreciation model: In this model, the investor receives a percentage of the home’s appreciation when it’s sold or refinanced. If the home’s value increases, the investor benefits from a portion of the gain.

- Share of home value model: Here, the investor receives a fixed percentage of the home’s current value when the agreement ends. This model focuses on the home’s value at the time of sale or refinance rather than just the appreciation.

Risk adjustment: Some investors apply a risk adjustment to the home’s appraised value. This adjustment reduces the home’s value by a certain percentage to account for potential market fluctuations and other risks.

For example, a company might apply a 5% risk adjustment to the home’s starting value. If your home appraises for $400,000, the risk-adjusted value would be $380,000, a $20,000 difference. This adjustment means you might receive less cash upfront and could owe more to the investor at the end of the agreement.

Can you pay back the equity share early?

“Some companies, including Unlock, offer homeowners the ability to buy their equity back in partial payments at any time during the term,” Micheletti says. “The percentage owed to the HEA provider is agreed upon up front and is calculated according to the home’s current value when a homeowner is ready to settle their agreement.”

Other investor groups might have specific conditions or fees associated with an early buyout. It’s important to read and understand these terms before signing the agreement to ensure it aligns with your financial goals and plans. Consult with a financial advisor before making an equity-share commitment.

What are the pros and cons of home equity sharing?

Micheletti says one of the biggest benefits of a home equity sharing agreement is that you can get the money you need without adding a new financial burden, and you’re not at the mercy of interest rates.

“Home equity sharing agreements are not debt. Unlike a home equity loan or home equity line of credit, you are not adding another bill to your monthly expenses,” he explains. “Because they are not loans, there are no worries about interest rates (and payments) changing, as is the case with most home equity lines of credit.”

Another benefit Micheletti shares with his clients is the ability to avoid losing your current low-rate mortgage.

“Home equity sharing doesn’t require homeowners to replace their mortgage as they would if they pulled equity from their home through a cash-out refinance. Someone who secured a very low rate a few years ago would not want to refinance into a mortgage at current rates.”

Below is an at-a-glance list of some of the key pros and cons to weigh before entering into a home equity sharing agreement.

Pros

- No monthly payments: You receive a lump sum of cash without the burden of monthly loan payments, providing financial flexibility.

- Shared risk: In many equity agreements, both you and the investor share the risk of your home’s value fluctuating, which can be beneficial in an uncertain market.

- Access to cash: Home equity sharing allows you to access a significant amount of cash for various needs, such as home improvements, debt consolidation, or other financial goals.

- Flexible qualification criteria: Since the agreement is based on the value of your home, not your credit profile, you may be able to qualify for a home equity sharing agreement with a credit score as low as 500 (depending on the provider).

- Improved credit score: Since there are no monthly payments, you can avoid the risk of missing payments and potentially improve your credit score.

- No additional debt: Unlike a loan, home equity sharing doesn’t add to your debt load, making it an attractive option for those wary of borrowing more money.

- Ideal for flexible income situations: Retirees and those with fluctuating incomes, such as self-employed and commissioned workers, are eligible.

- Fewer restrictions: In most cases, you can use the funds for any reason.

While these benefits can be helpful for many homeowners, Micheletti says the HEA path is not right for everyone.

“A home equity sharing agreement is likely not the best option for homeowners who are planning to move soon,” he cautions. “That is because you would want to give the home time to appreciate over the term of the agreement. That may not be a full 10 years — which is how long many home equity sharing agreement terms are – but it’s probably more than a couple of years.”

Cons

- Shared appreciation: You will share a portion of your home’s value or future appreciation with the investor, which could mean giving up a significant amount of your home’s value increase.

- Significant equity requirement: Most providers require homeowners to have at least 30% equity in their homes. If you don’t have this, you generally will not qualify for a home equity sharing agreement.

- Potential fees: Most equity sharing agreements include fees or costs that can reduce the amount of cash you receive.

- Long-term commitment: These agreements typically last for 10 to 30 years, so it’s a long-term financial commitment.

- Rigid draw structure: If you aren’t sure exactly how much of your equity you want to use (or when), you may be more comfortable with a home equity line of credit, in which you draw money from the credit line extended to you when you need it.

- Impact on future sales: When you sell your home, you must account for the investor’s share, which can impact your net proceeds.

- Complex setup: Understanding the terms and conditions of home equity sharing agreements can be complicated, requiring careful consideration and possibly legal advice.

- Limited availability: Home equity sharing agreements aren’t available to consumers in all states. You’ll need to check with different providers to see if they service your state.

When is a home equity sharing agreement a good option?

“Home equity sharing agreements are excellent options for homeowners who want to access the equity they have built up in their homes but without taking on additional monthly debt payments,” Micheletti says.

“They are also very good options for homeowners who may not qualify for a traditional loan product, like a home equity line of credit or home equity loan, because of their credit scores or income.”

According to Micheletti, some popular uses for home equity sharing funds include:

- Paying off high-interest debt (student loans, credit cards, personal loans, medical)

- Paying for home maintenance, repairs, renovations, remodels

- Funding education expenses

- Creating or building an emergency fund

- Covering large medical expenses

- Investing in rental or income property

- Contributing to retirement savings

- Financing or supporting a business

- Settling a divorce (property buyout)

- Diversifying or adding to an investment portfolio

“Homeowners who use their HEA proceeds to pay off high-interest debt may not only get ahead of bills but may also see an improvement in their credit scores,” Micheletti says.

Do you still own the home with an HEA?

“Home equity sharing agreements have no impact on a homeowner’s existing mortgage, enabling homeowners to live in their homes as usual,” Micheletti explains. “You retain the title to your property, along with exclusive rights of occupancy.”

In practice, this means you continue paying your mortgage, property taxes, and insurance like you normally would. The investor doesn’t live in the home or have any say in your day-to-day use of it. They only get involved later, when you sell, refinance, or reach the end of the agreement.

How much does a shared equity agreement cost?

Entering into a home equity sharing agreement involves various costs beyond the equity share that must be repaid to the investor. Here’s an overview of the potential expenses:

Transaction fees

Home equity sharing agreements typically include transaction or origination fees, which cover the costs associated with setting up and managing the agreement. These fees generally range from 3% to 5% of the total funding amount. For example, if you requested $80,000, your transaction fee might range from $2,400 to $4,000.

Third-party fees

Homeowners should also expect to pay third-party fees, similar to closing costs in a traditional mortgage. These can include:

- Appraisal fee: The average cost of a professional home appraisal typically ranges from $350 and $550, depending on your location and property. For larger or luxury homes, you might pay as much as $1,200.

- Home inspection: The average cost of a home inspection is between $296 to $424. Again, a larger or more complex property can have a higher inspection price.

- Title services: A standard title search usually runs from $75 to $200.

- Escrow services: These typically cost between $200 and $600.

These expenses are often deducted from the proceeds you receive from the equity sharing agreement, reducing the amount of cash available for your use.

Exit costs

When the term of the agreement ends, you may need to pay for another appraisal, home inspection, and title and escrow services. If you sell your property with a Realtor, you’ll also need to pay real estate commissions to your agent.

Compare before you commit: It’s a good idea to apply to multiple home equity sharing companies and consider other financing options, such as home equity loans, to get a clear picture of the short-term and long-term costs involved.

How can you get a home equity sharing agreement?

If you decide a home equity sharing agreement is a good fit for your situation, it’s time to find an investor service. Start by researching companies that offer this financing solution.

“Consumers can learn more about providers online,” Micheletti says. “It can be helpful to look at trusted review sites, such as Trustpilot or Better Business Bureau (BBB), to gain insights from customers about a provider you’re considering.” He adds that you’ll want to look for reputable providers with transparent terms.

Some established home equity sharing companies include:

- Unlock: unlock.com, 800-560-3450

- Unison: unison.com, 855-864-7664

- Hometap: hometap.com, 855-223-3144

- Point: point.com, 888-764-6823

- HomePace: homepace.com, 919-737-7637

While these are well-known companies with proven customer track records, others may not be as reputable.

As you research customer review websites, Micheletti cautions: “Be careful, as some sites may appear to be credible but are not. If you see ‘ad’ or ‘sponsored content,’ or other disclaimers, understand that the reviews are really paid advertisements.”

What to ask before signing an equity sharing agreement

Here are some questions to consider before you commit to a home equity sharing company.

- How much will the shared equity agreement cost?

- Are market conditions on my side?

- Will my current lender allow an equity sharing agreement?

- What term length is best for me?

- How much cash should I access?

- How soon can I get the funds?

- What are my repayment options?

- Can I make partial buy-out payments?

- Is there a cap on the final payback amount?

- What if I can’t repay the equity sharing investors?

- What are the tax implications of equity sharing?

- What happens if I die during the equity share term?

What are some home equity sharing agreement alternatives?

If home equity sharing doesn’t seem like the right fit for you or your home, consider these alternative options:

- Home equity loan: This more traditional loan allows you to borrow against the equity in your home with a fixed interest rate and monthly payments.

- Home equity lines of credit (HELOCs): A HELOC is a revolving line of credit secured by your property. This financing option lets you borrow as needed up to a certain limit. HELOCS typically have variable interest rates.

- Cash-out refinancing: This funding solution involves refinancing your current mortgage for a higher amount than you owe, taking the difference in cash.

- Reverse mortgages: Reverse mortgages are designed for homeowners aged 62 or older. This option allows you to convert a portion of your home’s equity into cash, with no repayment required until you sell the home, move, or pass away.

- Personal loans: These are unsecured loans that are popular for home improvements, debt consolidation, or other major expenses. They tend to have higher interest rates than secured loans.

- Home sale: If unlocking your home equity is a priority, and none of the financing alternatives above work for you, selling your house might be the best viable solution. This allows you to access all the equity you have built up in the property.

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.![]()

Unlock Your Equity and Buy Before You Sell

Is a home equity sharing agreement right for you?

Deciding whether a home equity sharing agreement is right for you depends on your financial situation, long-term goals, needs, and plans. It can be a unique way to get the money you need without the burden of monthly payments or the uncertainty that can come with high or variable interest rates.

As you weigh your options, keep in mind that you are taking on some risks with potential consequences. You are allowing the provider to hold a lien on your property. When the time comes, if you are unable to repay the home equity sharing agreement, the company can force you to sell your house to pay for its equity share. Discuss these risks with your financial advisor.

Micheletti offers this closing thought: “Finally, when considering ways to tap your home equity, keep in mind that it may be challenging to manage payments on both a mortgage and another loan, such as a home equity loan or home equity line of credit. Missing payments on the main mortgage or the home equity-based loan can risk foreclosure. In contrast, the home equity sharing agreement carries no monthly debt payments.”

Editor’s note: This post is meant for educational purposes, not financial advice. If you need assistance navigating home equity sharing agreements, HomeLight encourages you to reach out to your own financial advisor.

Header Image Source: (Curtis Adams/ Pexels)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.