What are Home Equity Sharing Companies?

- Published on

- 15 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

Home equity sharing companies offer an innovative way to leverage your home’s equity without taking out a loan or making additional monthly payments.

If you can’t afford or qualify for a traditional home equity loan, this financing option may be a solution to quickly access cash for a life change or opportunity.

However, working with a home equity sharing company involves some risks that you’ll want to understand and weigh.

How Much Is Your Home Worth Now?

Home values have rapidly increased in recent years. How much is your current home worth now? Get a ballpark estimate from HomeLight’s free Home Value Estimator.

Editor’s note: This post is meant for educational purposes, not investment advice. If you need assistance navigating home equity sharing companies, HomeLight always encourages you to reach out to your own financial advisor.

What is home equity sharing?

Home equity sharing is a financial arrangement where a company invests in your home in exchange for a percentage of its future value. Instead of taking out a traditional loan, you partner with a company that provides you with a lump sum of cash. In return, the company shares in the appreciation (or depreciation) of your home’s value when you sell or refinance.

This alternative financing option is appealing because it doesn’t require monthly payments or accrue interest. It’s a way to unlock your home’s value while avoiding additional debt.

Depending on your situation, a home equity sharing agreement might also be an option to get cash for a down payment on a house. However, there are a number of factors to consider, and this path is not for everyone.

How does home equity sharing work?

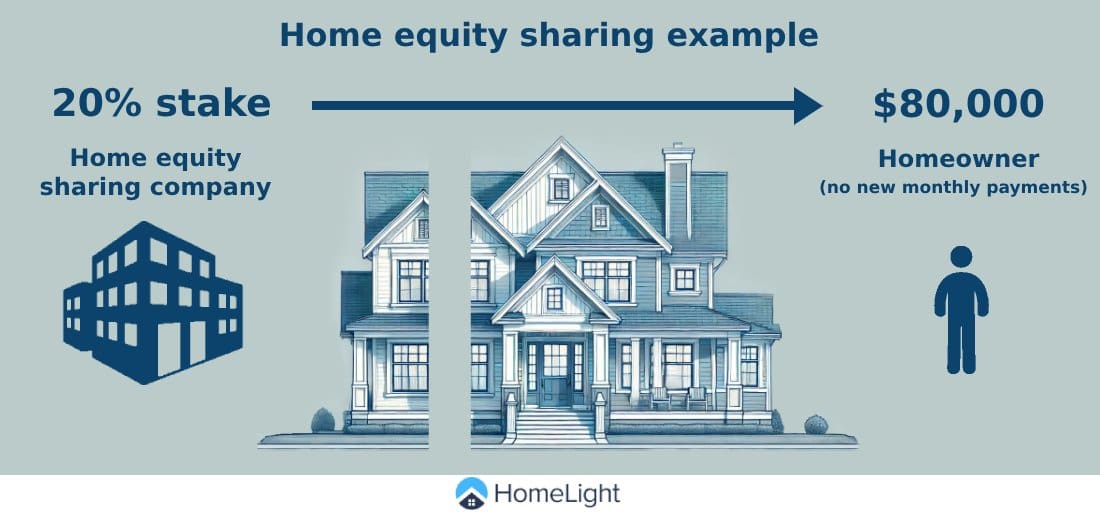

Let’s look at an example of how a home equity sharing agreement might work. For clarity, we’ll use a $400,000 home value. This could be how much your paid-off home is worth, or how much equity stake you own in the property.

If an investment company buys a 20% stake in your home equity and your home is worth $400,000, it would give you a $80,000 lump sum.

- Your home’s current value: $400,000

- Amount of cash you need: $80,000

- Investment company’s stake: 20%

- Home equity sharing contract term: 10 years

- Home’s annual appreciation rate: 3%

At the end of 10 years, the home appreciates to approximately $537,566. The homeowner will need to pay back the original investment ($80,000) plus the investor’s 20% stake in the home’s $137,566 appreciation amount ($27,513). In this case, the payback amount would be about $107,513.

Below is a table that shows the breakdown of this home equity sharing scenario, and what happens if, for some reason, the home depreciates in value — since it is an investment venture, after all.

| If your home appreciates | If your home depreciates | |

| Starting home value | $400,000 | $400,000 |

| Home value at repayment | $537,566 | $380,000 |

| Total increase/decrease | $137,566 | -$20,000 |

| Shared equity percentage | 20% (for gain of $27,513) | N/A (loss of $20,000) |

| Original funding amount | $80,000 | $80,000 |

| Amount you owe the investor | $107,513 | $60,000 |

What if your home depreciates in value?

A common question about home equity sharing companies is what happens if your home loses value. With home equity sharing, the company shares in both the appreciation and depreciation of your property.

If your home’s value decreases, the amount you owe the company will also decrease. As shown in the example above, if your home’s value drops from $400,000 to $380,000 and the company has a 20% equity share, it would receive $60,000 instead of the original $80,000.

Repayment note: How much you owe at the end of your home equity sharing agreement will depend on the terms you agreed to. Repayment requirements vary by company. Our example above illustrates a common model, but you might have a different agreement based on a percentage of your home’s ending value.

Steps to work with a home equity sharing company

The process typically involves the following steps:

1. Vet home equity sharing companies: You’ll first need to identify a home equity sharing company that serves your area. Be certain it has a solid reputation. We’ll provide a list of top home equity sharing companies later in this post.

2. Initial consultation: Your next step is a consultation to determine if home equity sharing is a good fit for you. The company will assess your home’s value and your financial situation. You’ll need a sufficient amount of equity.

3. Agreement terms: If you and your home qualify, the company will present an offer outlining the terms, including the percentage of equity they’ll share and the amount you’ll receive. You’ll want to pay close attention to the payback requirements.

4. Signing the agreement: Once you agree to the terms, you’ll sign the contract. The company will then provide you with the agreed-upon funds.

5. Use of funds: You can use the funds for any purpose, such as home improvements, debt consolidation, college tuition, a downpayment on another home, or other major expenses.

6. Future sale or refinance: When you sell or refinance your home, you’ll repay the company based on the current value of your home. The repayment amount includes the company’s share of any appreciation or depreciation.

Examples of home equity sharing companies

Unison

Website: unison.com

Phone: 415-992-4200

Founded in 2004, Unison is a San Francisco and Omaha-based investment company that offers home equity sharing in 29 states and Washington, D.C. The company invests up to 15% of your home’s current value in exchange for cash and a share in the appreciation or depreciation of your property value. Investment amounts range from $30,000 to $500,000.

What sets Unison apart is its extended 30-year term option. To settle your agreement with Unison, you can opt for a buyout, sell your house, or refinance within 30 years. However, if you choose a buyout, Unison will not share in any loss of value.

Additionally, there is an initial five-year period during which Unison does not share in any loss if you sell your property. It’s important to note that Unison restricts renting out your home during this term. The company also charges a transaction fee and an appraisal fee.

Unison’s process starts with you requesting a near-instant online estimate of your equity potential. The application takes about two minutes, and then an appraisal determines how much equity you can unlock.

Hometap

Website: hometap.com

Phone: 855-223-3144

Founded in 2017, Hometap is a Boston-based fintech company dedicated to making homeownership more accessible and less stressful. Their mission is to help you get more out of your home so you can get more out of life.

Hometap typically works with homeowners who have a credit score of 600 or higher, though you can qualify with a score as low as 500, albeit with less favorable terms. The maximum investment amount from Hometap is $600,000, which can be available in as little as three weeks.

A downside is the lack of flexibility in buyout options, with a maximum term of 10 years and strict repayment requirements. An upside is that there are no prepayment penalties, so you can buy out the investment at any time with savings, a refinance, or the sale of your home. As with most home equity sharing companies, Hometap does not require monthly payments.

Point

Website: point.com

Phone: 888-764-6823

Based in Palo Alto, California, and operating since 2015, Point offers home equity sharing options for homebuyers and homeowners, as well as home HELOCs. Point operates in 23 states and Washington, D.C., providing flexible financial solutions for accessing your home equity.

Through Point’s shared equity agreement, you can access between $25,000 and $500,000 of your home equity, with your choice of term lengths up to 30 years. Unlike a traditional loan, a lower credit score won’t disqualify you from an equity unlock. With Point, you can qualify for a home equity sharing agreement with a credit score of just 500 or higher.

While Point charges a processing fee and appraisal fee, these don’t need to be paid upfront. For a premium fee, Point also allows investments in rental properties.

Additionally, Point has a waiting list for a new financing product called SEED, a partnership between homebuyers and Point. As a buyer, you can get funds to increase your down payment to 20% (or more) in return for a portion of your home’s future appreciation. This can lower your monthly payment and help you avoid the need for private mortgage insurance (PMI).

Unlock

Website: unlock.com

Phone: 800-560-3450

Established in 2020 and based in San Francisco, Unlock is one of the newer home equity sharing companies in the U.S. Unlock offers home equity agreements with terms up to 10 years and amounts up to $500,000, with no interest charges or monthly payment requirements. This flexibility allows you to pay off high-interest debt, make home improvements, or fund a child’s education without the burden of additional payments.

Despite being somewhat new to the home equity sharing arena, Unlock has already assisted more than 7,000 homeowners. The application process starts online, but you’ll have a dedicated home equity consultant to assist you from appraisal to receiving funds.

Unlock states upfront that it is not a lender or a bank but a team of consumer finance, mortgage, and real estate leaders aiming to help homeowners who have been overlooked by traditional finance systems. The company’s primary goal is to enable you to access home equity without taking out a traditional loan, giving you more control over your finances.

HomePace

Website: homepace.com

Phone: 919-737-7637

Founded in 2020 and based in Park City, Utah, HomePace specializes in helping homeowners access their equity through home equity agreements. HomePace’s mission is to address the growing need for financial flexibility by providing Americans with more options to access capital without incurring debt.

HomePace will purchase up to 15% of your home’s equity, allowing you to receive up to $250,000 in upfront cash. The company offers a 15-year term length, which is five years longer than many other home equity sharing companies, providing you with more flexibility for buyouts.

Like other equity sharing agreements, you won’t make monthly payments. Repayment is due only after you sell the house, refinance, or after the 15-year term, whichever comes first.

HomePace operates in six states: Arizona, Colorado, North Carolina, Tennessee, Utah, and Washington. The company charges an origination fee, deducted from the funds you receive, so there are typically no out-of-pocket expenses. To be eligible, you must have a credit score of at least 630, which is higher than other companies.

Benefits of home equity sharing

Home equity sharing offers several advantages that make it an attractive option for many homeowners. Here are some key benefits:

- No monthly payments or interest: With home equity sharing, you don’t have to worry about monthly payments or accruing interest. This can significantly ease your financial burden compared to traditional loans or lines of credit.

- Access to cash without high interest: By partnering with a home equity sharing company, you can access a lump sum of cash without the high interest rates typically associated with loans and mortgages.

- No new loan: Home equity sharing doesn’t involve taking on new debt. Instead, you receive cash in exchange for a share of your home’s future value.

- Fewer qualification hurdles: Many home equity sharing companies have less stringent qualification requirements than traditional lenders, making it easier for homeowners with varying credit profiles to qualify.

- No use restrictions: The funds you receive from a home equity sharing agreement can be used for any purpose, whether it’s home improvements, debt consolidation, education expenses, or other financial needs.

- You can stay in your home: Unlike some fast-cash solutions that involve selling your home quickly, home equity sharing allows you to remain in your home while accessing its equity.

- Can be faster than a loan: The process of securing funds through home equity sharing can be quicker than traditional loan approval processes, allowing you to access needed funds more rapidly.

- Shared risk: Home equity sharing agreements mean that the company shares in both the appreciation and depreciation of your home’s value, which can provide some peace of mind in fluctuating markets.

Drawbacks of home equity sharing

While home equity sharing has its benefits, there are also some drawbacks to consider:

- Less profit from home appreciation: By entering into a home equity sharing agreement, you agree to give up a portion of your home’s future appreciation, which means you might receive less profit when you sell.

- You’ll need sufficient equity: To qualify for home equity sharing, you need to have a significant amount of equity in your home. This option may not be suitable for homeowners who have recently purchased their property or have little equity built up.

- More complex than a loan: Home equity sharing agreements can be more complex than traditional loans, requiring careful review and understanding of the terms and conditions.

- Exit strategies can be bumpy: Exiting a home equity sharing agreement can sometimes be complicated, especially if the value of your home has changed significantly or you encounter an unexpected life change. You’ll need to plan your exit strategy carefully.

- Limited availability: Home equity sharing is not available in all states or regions, so your options may be limited based on your location. In addition, your existing mortgage provider or state laws may prohibit you from entering into a home equity sharing agreement.

- Can impact future selling plans: Because the company shares in the future value of your home, your plans to sell or refinance could be impacted. You’ll need to consider how the agreement aligns with your long-term goals.

- Potential for higher total cost: Depending on how much your home appreciates, the total cost of a home equity sharing agreement could end up being higher than a traditional loan or mortgage.

Unlock Your Equity and Buy Before You Sell

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

Things to consider when selecting a company

When choosing a home equity sharing company, it’s important to evaluate several factors to ensure it meets your needs:

- Qualification requirements: Check the company’s qualification criteria to ensure you meet their requirements. This can include credit score, equity levels, and other financial health indicators.

- How much you’re able to borrow: Different companies have varying limits on how much equity they will invest. Make sure the amount you can access fits your financial needs.

- Term length: Consider the length of the term for the home equity sharing agreement. Longer terms can provide more flexibility, while shorter terms may be suitable for those with specific financial plans.

- Service availability: Verify if the company operates in your state or region. Availability can vary, so it’s important to choose a company that serves your area.

- How long it takes to receive funds: The time it takes to receive funds can vary between companies. If you need cash quickly, look for a company known for a fast approval and funding process.

- Repayment options: Understand the repayment terms and options. Some companies may offer more flexible repayment strategies, while others might have stricter conditions.

- Fees you’ll need to pay: Be aware of all fees associated with the agreement, including transaction fees, appraisal costs, and any other charges. These can impact the overall cost of the agreement.

Other home equity sharing company considerations

In addition to the pros, cons, and company vetting points we’ve discussed, here are 10 key aspects to consider before signing a home equity sharing agreement (HEA):

- Existing mortgage constraints: Check your current mortgage agreement for any restrictions or penalties related to HEAs. Some lenders may impose fines or require immediate full repayment of the loan balance (an acceleration clause) when you enter into a HEA.

- Consultation with a financial advisor: Given the complexities and potential implications of an HEA, it is wise to consult with a financial advisor to understand how it fits with your financial situation and goals.

- Partial buy-out payments: Ask if the home equity sharing company allows for partial buy-out payments. This option can provide more flexibility by enabling you to repay in smaller amounts over time rather than a lump sum at the end of the term.

- Maximum repayment cap: Carefully read the HEA to see if there’s a cap on the final payback amount. A cap can protect you from excessively high repayments if your home significantly increases in value.

- Repayment inability: Be aware of the consequences if you’re unable to repay the home equity sharing investors. This could lead to the forced sale of your home to cover the debt.

- Long-term financial goals: Consider how an HEA fits into your long-term financial plans. While it provides short-term liquidity, it may reduce your net proceeds from a future home sale.

- Market conditions: Real estate market trends can affect your home’s future value and, consequently, the amount you’ll owe. A rising market may increase your repayment amount, while a declining market might reduce it.

- Tax implications: HEAs can have different tax implications compared to traditional loans. Consult a tax advisor to understand how an HEA might affect your tax situation.

- Contract terms and conditions: Every HEA is unique. Pay close attention to the details, including the percentage of equity the company will hold, the term length, and any other specific conditions.

- If a homeowner dies: If the homeowner passes away, the estate must honor the terms of the HEA. Any heirs will need to divide the proceeds from any gains or share in any losses.

Home equity sharing company alternatives

If home equity sharing doesn’t seem like the right fit for you, consider these alternative options:

- Home equity loans: These are traditional loans where you borrow against the equity in your home. They come with fixed interest rates and regular monthly payments.

- Home equity lines of credit (HELOCs): A HELOC is a revolving line of credit secured by your home. It allows you to borrow as needed up to a certain limit, with variable interest rates.

- Cash-out refinancing: This involves refinancing your existing mortgage for a higher amount than you currently owe, taking the difference in cash.

- Reverse mortgages: Available to homeowners aged 62 or older, a reverse mortgage allows you to convert part of your home equity into cash, with no repayment required until you sell the home, move out, or pass away.

- Personal loans: These unsecured loans can be used for various purposes, including home improvements, debt consolidation, or other significant expenses. They typically have higher interest rates than secured loans.

- Selling your home: If accessing your home equity is a priority and none of the financing options work for you, selling your home might be a viable alternative. This allows you to unlock all the equity you have built up.

Is using a home equity sharing company right for you?

Deciding whether home equity sharing is the right choice for you depends on your unique financial situation, goals, and needs. It can be an excellent way to access cash without the burden of monthly payments or high interest rates, especially if you have significant home equity and a solid plan for how to use the funds.

As you weigh your options, think about how a home equity agreement fits into your broader financial picture. Consider these four self-assessment questions:

- Will entering into a home equity sharing agreement align with my family’s goals?

- Am I planning on staying in this house for the life of the HEA term?

- How might market fluctuations affect the outcome I’m hoping for?

- Am I comfortable with the shared risk and reward model of a home equity sharing agreement?

It’s crucial to consider these questions and any potential drawbacks, such as reduced profits from home appreciation, the complexity of these agreements, and the consequences if you are unable to repay the home equity sharing company when the time comes.

Evaluate your options carefully, consult with financial and tax advisors, and thoroughly review the terms and conditions of any home equity sharing agreement.

Header Image Source: (Salman Saqib/Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.