What Is a Good Mortgage Rate to Buy a House?

- Published on

- 14 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorClose Richard Haddad Executive Editor

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

Buying a home is exciting, but securing a good mortgage rate can be challenging, especially when the housing market feels unsettled or unpredictable. But when you’re shopping for a home, what is a good mortgage rate?

In this guide, we’ll explain what influences mortgage rates and what might qualify as a “good” rate based on historical trends and your goals as a homebuyer. We’ll also outline some steps you can take to help you secure the best deal possible.

Discover How Much Home You Can Afford With Our Home Affordability Calculator

Understand the costs associated with buying a home and find out what safe budgeting looks like.

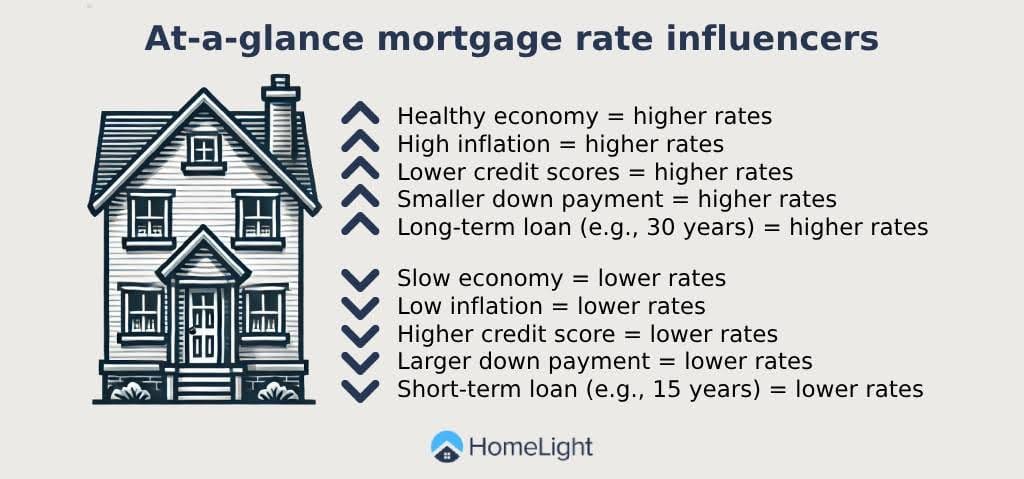

What factors influence mortgage rates?

Let’s take a quick look at the mix of economic and personal factors that influence mortgage rates on a home loan:

- Federal Reserve policies: The Federal Reserve doesn’t directly set mortgage rates, but its actions to control inflation through short-term interest rate adjustments significantly impact mortgage rate trends.

- Economic conditions: When the economy is thriving, mortgage rates tend to rise as borrowing demand increases. In contrast, rates often drop when the economy slows. In recent years, the market has generated confusing economic indicators that have been tricky for economists to interpret.

- Inflation: Mortgage lenders set rates to keep pace with inflation. High inflation usually drives rates up, while lower inflation typically keeps them down.

- Loan amount and down payment: Borrowers with larger down payments and smaller loan amounts may receive more favorable rates because lenders view these loans as less risky.

- Credit score: Borrowers with higher credit scores typically qualify for lower rates, as lenders consider them more likely to repay on time.

Here are a few additional factors that can play a role in mortgage interest rates:

- Employment and wage trends: Strong job growth and rising wages can lead to higher mortgage rates, as these indicate a healthy economy with greater borrower demand.

- Global events: Events like international conflicts, supply chain disruptions, and global economic slowdowns can impact U.S. mortgage rates, as they often influence investor behavior.

- Lender competition: Rates may vary slightly depending on the competitiveness of your local mortgage market. Lenders offer better rates to attract more borrowers in highly competitive areas.

- Loan term: A shorter loan term (e.g., 15 years) typically comes with lower interest rates than a standard 30-year mortgage due to faster repayment schedules.

- Loan type: Conventional, FHA, VA, and USDA loans may all offer different rates due to varying eligibility criteria, fees, and government guarantees.

What is a good mortgage rate?

The definition of a “good” mortgage rate will vary depending on the current economic climate, your financial situation, and your individual needs and goals. Ultimately, a good mortgage rate depends on what’s available and achievable for you.

“The lowest rate is not always the best rate, although it might seem like it,” says Richie Helali, a mortgage specialist at HomeLight. “When purchasing a home, it’s more about finding the right home vs. the day-by-day rate. There are always lower rates available; however, they come with an additional upfront cost — purchasing mortgage points.”

Helali explains that mortgage points are a form of prepaid interest. “These points are charged upfront as part of closing costs to ‘buy down’ an interest rate. It’s best to discuss with your loan officer if paying points for a lower rate is worth it or not.”

In the current market, Helali says getting what you consider a good mortgage rate may be more likely after you secure the home you want.

“Chances are, anyone who is purchasing now or has purchased a home within the last two or three years will be refinancing to a lower rate within the next year or so,” he, says. “It might make paying points upfront for a lower rate more expensive than taking the current rate and refinancing later on.”

Real estate agents often describe this home-buying strategy as “Marry the house, date the rate.” This approach encourages buyers to focus on buying a home they love with the best available mortgage interest rate, and then breaking up with the rate later when it makes sense to refinance.

Curious about how much home you can afford? Try HomeLight’s free Home Affordability Calculator, which lets you factor in additional costs such as property taxes, insurance, and HOA fees.

What good mortgage rates do buyers want?

According to a recent survey, most Americans say a good 30-year fixed mortgage rate is 4% or below. While not realistic in the current market, this mindset is likely influenced by the fact that thousands of U.S. homeowners refinanced at record-low 2.6%-4% rates during the pandemic era (2020 and 2021).

Data from the CNET survey reveals that half of U.S. adults say a mortgage rate of 4% or below would make them “realistically consider” purchasing a home. Of those, 20% would still consider buying a house if rates fell between 4.5% and 5.5%. Only 4% say they would consider buying at a 6% rate. Here’s a breakdown of the CNET survey results:

- 6.5% rate or below: 2% of adults would consider buying

- 6% rate or below: 2% of adults would consider buying

- 5.5% rate or below: 5% of adults would consider buying

- 5% rate or below: 9% of adults would consider buying

- 4.5% rate or below: 6% of adults would consider buying

- 4% rate or below: 26% of adults would consider buying

A surprising 29% of adults say there is no mortgage rate that would allow them to realistically consider buying or refinancing a home right now, no matter the interest rate. Another 21% say they aren’t sure. However, 45% of U.S. adults say lower home prices would play a role in their decision to purchase a home.

What mortgage rates do most U.S. homeowners hold?

Based on a HomeLight review of the most recent nationwide data, more than half of all U.S. homeowners with an outstanding mortgage have a rate of 4% or lower. Here is a simplified snapshot of the current mortgage rate breakdown:

- 22% of current U.S. mortgage holders secured rates below 3%.

- 34% pay between 3% and 4%.

- 18% have rates from 4% to 5%.

- 10% pay between 5% and 6%.

- 16% hold rates above 6%.

If you’re shopping today, a rate as attractive as 3% to 6% will likely be hard to find unless you’re assuming a mortgage loan. But as Helali points out, the focus should be on finding a home you love, you can always refinance later. Let’s take a moment to look back to see why today’s interest rates may qualify as a good mortgage rate.

How do today’s mortgage rates compare with history?

Glancing back at interest rates through the decades can provide valuable perspective in your quest to determine a good mortgage rate. The average 30-year rate since 1971 is 7.73%. Using data from Freddie Mac, here’s a look at what our parents or grandparents paid for their home loans.

Mortgage interest rates 1974-2024

| Year | Average 30-year rate | Year | Average 30-year rate | Year | Average 30-year rate | Year | Average 30-year rate |

| 1974 | 9.19% | 1987 | 10.21% | 2000 | 8.05% | 2013 | 3.98% |

| 1975 | 9.05% | 1988 | 10.34% | 2001 | 6.97% | 2014 | 4.17% |

| 1976 | 8.87% | 1989 | 10.32% | 2002 | 6.54% | 2015 | 3.85% |

| 1977 | 8.85% | 1990 | 10.13% | 2003 | 5.83% | 2016 | 3.65% |

| 1978 | 9.64% | 1991 | 9.25% | 2004 | 5.84% | 2017 | 3.99% |

| 1979 | 11.20% | 1992 | 8.39% | 2005 | 5.87% | 2018 | 4.54% |

| 1980 | 13.74% | 1993 | 7.31% | 2006 | 6.41% | 2019 | 3.94% |

| 1981 | 16.63% | 1994 | 8.38% | 2007 | 6.34% | 2020 | 3.10% |

| 1982 | 16.04% | 1995 | 7.93% | 2008 | 6.03% | 2021 | 2.96% |

| 1983 | 13.24% | 1996 | 7.81% | 2009 | 5.04% | 2022 | 5.34% |

| 1984 | 13.88% | 1997 | 7.60% | 2010 | 4.69% | 2023 | 6.81% |

| 1985 | 12.43% | 1998 | 6.94% | 2011 | 4.45% | 2024 | 6.1%- 6.8%* |

| 1986 | 10.19% | 1999 | 7.44% | 2012 | 3.66% | 2025 | TBD |

Source: Freddie Mac (*2024 estimated average range as of October 31)

More perspective on what is a good mortgage rate: In 1981, the average 30-year mortgage rate was 16.63%, but rates peaked at 18.63% in October of 1981. If you purchased a home with a $400,000 loan at 18.63%, you would pay a monthly payment of $6,234.

How can I get a good mortgage rate?

Securing a favorable mortgage rate is achievable with planning, preparation, and strategy.

“Some of the biggest factors are the percentage you put down and your credit score. In both cases the more, the better,” Helali, says, adding that “It’s always best to shop around for the best rate and terms. As a general rule of thumb, get a rate quote from at least three or four mortgage lenders before committing.”

When shopping for a good mortgage rate, Helali suggests you request three quotes from each lender:

1. Current rate with regular closing costs

2. Lower rate with increased closing costs (paying down points)

3. Higher rate with little to no closing costs

“Mortgages with higher rates usually come with lower or no closing costs,” Helali says.

Here are some steps you can take to help get the best rate possible:

- Improve your credit score: A higher credit score can significantly lower your interest rate. Pay off outstanding debts, reduce your credit card balances, and avoid opening new credit accounts before applying for a mortgage.

- Increase your down payment: The more you put down, the less risky your loan appears to lenders. A larger down payment can help you qualify for lower rates and reduce your monthly mortgage payments.

- Shop around: Mortgage rates can vary widely among lenders, so it pays to get multiple quotes. Request rate estimates from different lenders and compare the terms and fees associated with each offer.

- Negotiate with lenders: Don’t hesitate to negotiate! Some lenders are willing to offer lower rates or reduce closing costs to win your business. Ask if they can match or beat any competitive offers you’ve received.

- Consider mortgage points: Points are upfront fees you pay at closing to lower your mortgage rate. One point typically costs 1% of the loan amount and reduces your interest rate by a set amount. This option may be worthwhile if you plan to stay in your home long-term.

- Choose a shorter loan term: While monthly payments are higher, shorter-term loans (like 15-year fixed loans) generally have lower interest rates than 30-year loans.

Interest rate vs. APR

As you shop around for a good mortgage rate, it’s helpful to understand the difference between the loan’s interest rate and the annual percentage rate.

- Interest rate: The interest rate is the percentage charged on your mortgage loan principal. It reflects the cost of borrowing but does not include other fees.

- APR (Annual Percentage Rate): APR includes the interest rate and additional lender fees, such as closing costs and origination fees. The APR offers a more complete picture of the loan’s overall cost. When comparing loans, the APR reflects what you’ll pay beyond the interest.

How much mortgage interest will I pay?

To give you an idea of mortgage interest costs, here’s a sample breakdown for a $400,000 home loan with a 6% interest rate over a 30-year term:

- Loan amount: $400,000

- Interest rate: 6%

- Monthly principal and interest payment: approximately $2,398

Over the life of this loan, you’d pay around $463,000 in interest alone, bringing the total cost of the mortgage to about $863,000. Keep in mind that a lower interest rate will reduce both your monthly payment and total interest costs, which is why securing a good rate is so significant.

FAQs about good mortgage rates

Discount points are fees you can pay upfront to lower your mortgage’s interest rate. One point typically equals 1% of the loan amount and can reduce the interest rate by around 0.25%. If your loan is $200,000, one point would cost $2,000 and lower your interest rate by 0.25%. This option of buying down the rate might make sense if you plan to stay in your home for a long time, as the upfront cost can pay off over the loan’s duration.

You can generally refinance a mortgage after six or seven months, though it varies by lender and loan type. However, it’s essential to consider if the current rates and fees justify the refinancing costs. Refinancing may help you lower your interest rate, reduce your monthly payment, or adjust your loan term.

When it comes to refinancing, Helali says the top things you should consider are rates and fees. “The longer you wait to pull the trigger the better. If you’re itching to refinance now because the current rate is lower, consider asking your loan officer for a ‘no closing cost’ refinance as a comparison. Depending on when you refinance, it might be a good option.”

If your down payment is less than 20%, most lenders will require private mortgage insurance (PMI) to protect against default risk. PMI adds to your monthly payments but can often be canceled once you reach 20% equity in your home. FHA loans and certain other types of loans also require mortgage insurance, which may be permanent depending on the loan terms.

Locking in your mortgage rate can protect you from potential rate increases before closing. Most rate locks last 30 to 60 days, with some flexibility. If rates are expected to rise, a lock-in can offer peace of mind. However, if the market suggests a downward trend, you might consider waiting to lock in, depending on your closing timeline and risk tolerance.

“A seasoned loan officer can help walk borrowers through when it may be a good time to lock, and when it’s better to wait before locking a rate,” Helali says. “Keep in mind that the vast majority of mortgage lenders cannot ‘unlock’ a rate. Once you lock, you’re subject to those terms for better or for worse.”

Yes, some mortgage products carry more risk. Adjustable-rate mortgages (ARMs), for example, offer low introductory rates that later adjust based on market rates, potentially leading to higher payments. Interest-only loans and balloon mortgages also have riskier structures, often appealing in the short term but with unpredictable payments over time.

No, mortgage lenders vary in their offerings, rates, fees, and service quality. It’s important to compare lenders to ensure you’re getting the best terms for your financial situation. Local banks, national lenders, and credit unions all offer different benefits and trade-offs. Working with a reputable lender who prioritizes transparency can make the process smoother.

Partner with a top agent for the most value

Navigating mortgage rates is just one part of a successful home purchase. For the rest, having an experienced real estate agent by your side can make a big difference. A top agent can guide you through the home-buying process, negotiate on your behalf, and help you make strategic choices from start to finish.

With HomeLight’s free Agent Match platform, you can find a qualified agent with proven results in your area. Connect with a top-performing real estate agent today to start your journey toward finding your dream home — and securing the best mortgage possible.

Header Image Source: (Curtis Adams/ Pexels)

- "If I am considering an adjustable-rate mortgage (ARM), what should I look out for in the fine print?", Consumer Financial Protection Bureau (February 2024)

- "Most Homebuyers Won't Budge Until Mortgage Rates Drop to 4%, CNET Survey Finds", CNET (November 2024)

- "Data Spotlight: The Impact of Changing Mortgage Interest Rates", Consumer Financial Protection Bureau (September 2024)

- "How does inflation affect mortgage rates?", Yahoo! (September 2024)

- "America’s economy is wildly confusing right now. Here’s what’s really going on", CNN Business (August 2024)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.