How Do I Find a Home With an Assumable Mortgage?

- Published on

- 14 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

For many buyers curious about how to find assumable mortgages, the search is like a dual treasure hunt. You’re browsing homes for sale, searching for the perfect fit for your budget, and at the same time, trying to find out if the seller’s loan is assumable.

But if you succeed in the search, you can sidestep today’s high mortgage interest rates and secure a monthly payment that could be hundreds of dollars less. Because of these golden benefits, assumable loans are in demand. Along with the obvious advantage of a lower interest rate, an assumed loan can come with fewer transaction fees and greater speed.

Partner With a Top Agent Familiar With Assumable Mortgage Listings

HomeLight can connect you with a top-performing real estate agent who understands the ins and outs of assumable mortgage listings in your market.

“Assuming an existing mortgage can save you on closing costs,” says Eric Broesamle, a top Michigan real estate agent who works with nearly 74% more single-family homes than the average agent in his Mount Clemens market. “There are typically fewer fees involved when you do an assumable mortgage rather than a new origination. Plus, the approval process can be faster.”

In this post, we’ll explain how this often elusive financing option can work for you, and share expert tips on how to find an assumable mortgage attached to a home you want to buy.

What is an assumable mortgage?

An assumable mortgage is a unique arrangement where a homebuyer has the opportunity to take over the seller’s existing mortgage. This type of financing is increasingly popular among buyers who wish to benefit from lower interest rates.

In the current real estate market, many sellers listing their homes refinanced their mortgages during historically low pandemic-era rates, when rates fell to an all-time low of 2.65%.

Taking on an assumable mortgage can seem like stepping into a financially advantageous position. Instead of securing a new mortgage with higher rates, a buyer can assume the home seller’s existing interest rate, principal balance, repayment period, and other terms of the lending agreement.

“A lot of people right now are concerned about interest rates,” says Broesamle. “This is a great feature for my clients when they’re looking to purchase a new home, and a lot of them don’t know that this is an option.”

It’s important to note, however, that not every mortgage is assumable. Buyers interested in this option must be aware of certain criteria, qualifications, and fees that can come with assuming a mortgage.

What types of mortgage loans are assumable?

Identifying assumable mortgage loans involves examining the type of loan and its specific conditions. Generally, government-backed or insured loans are the most common assumable loans. Here’s a brief overview of assumable mortgage types:

- FHA Loans: FHA loans, backed by the Federal Housing Administration, are often assumable, subject to lender approval. A qualified buyer must meet standard FHA loan requirements, such as a minimum credit score of 580 and a 3.5% down payment.

- VA Loans: VA loans, guaranteed by the Department of Veterans Affairs (VA), are usually assumable, and many VA homeowners have a mortgage rate below 5%. Assumption eligibility includes a minimum 620 credit score and VA approval. Notably, non-veterans can also assume these loans, with the key determinant being creditworthiness. A VA loan comes with the standard 0.5% funding fee.

- USDA Loans: Assumable under certain conditions, USDA loans typically require approval from the lender and the United States Department of Agriculture (USDA). The assumption often results in a new interest rate and terms, although exceptions exist, such as in family transfers, where the original rate and terms may be retained without the borrower meeting all the USDA eligibility requirements.

- Some jumbo loans: Some jumbo mortgages that are originated by larger banks and not sold to Fannie Mae and Freddie Mac can be assumed. These circumstances are uncommon, however, and it can be difficult to know which jumbo mortgages are assumable.

- Some Adjustable-Rate Mortgages (ARMs): Certain ARMs can be assumable, allowing the new buyer to take over the existing rate and terms. It’s important to note that assuming an ARM may involve relinquishing the option to convert it into a fixed-rate mortgage. In cases where a conventional ARM loan has been deferred or modified to help the borrower avoid default, the loan is likely not eligible to be assumed.

Conventional loans are typically not assumable

Conventional mortgages, particularly those backed by Fannie Mae and Freddie Mac, are generally not assumable. These loans usually have a “due on sale” or “due on transfer” clause, requiring full repayment when the original borrower sells the home.

However, in certain special circumstances, such as after a death or divorce, some conventional loans may become assumable. For this to be possible, the mortgage contract must include an “assumption clause.” This clause permits the transfer of the loan to another party. Despite this provision, lender approval is still required, and the new borrower must meet the original loan’s eligibility criteria.

How do I find an assumable mortgage?

Finding a home with an assumable mortgage takes some extra digging and a bit of patience. It’s not an easy or fast search, but it can be well worth your efforts. Here are some ways to locate these types of listings:

1. Partner with an experienced agent

An experienced real estate agent, particularly one familiar with assumable mortgages, can be invaluable. They often have access to listings and networks that may not be publicly available, allowing them to identify homes with assumable mortgages more quickly.

“Finding the property initially is probably the most important part. Your agent can search for listings with assumable loans,” says Broesamle, who’s been helping home shoppers for more than 20 years.

“Once you find the home you like, you need to reach out and talk to the seller’s agent and work with the seller in order to find out who their loan company is to make sure that you can assume the loan.”

If you’re still on the hunt for a great real estate agent, HomeLight’s Agent Match tool can help you find top-rated local experts.

2. Search real estate websites using keywords

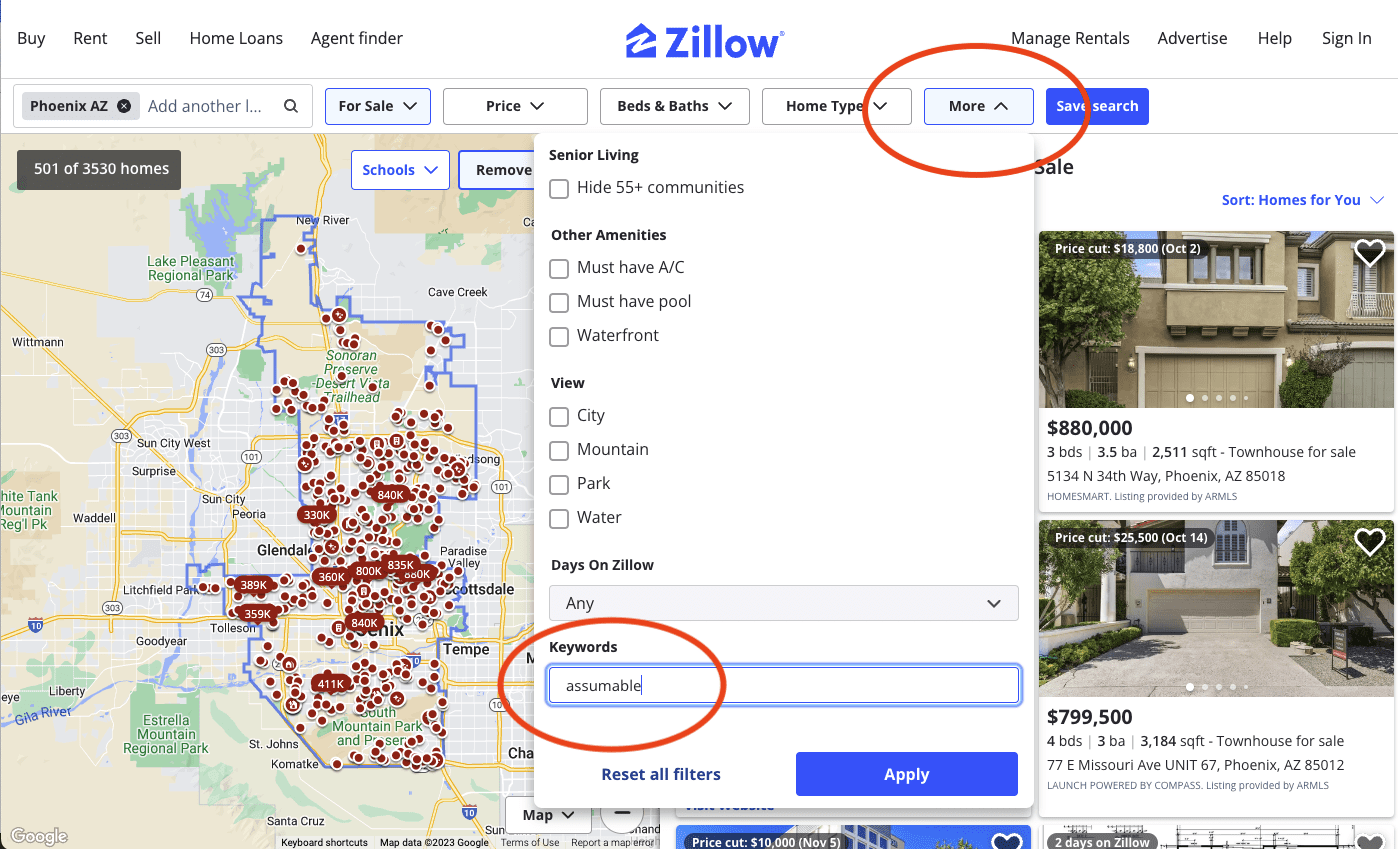

Assumable mortgages are gaining attention among homebuyers, with more real estate listings on platforms like Redfin and Zillow highlighting the option to take over an existing loan.

Most websites have advanced filtering options that will let you enter keywords into your home search. If the seller or their agent is aware that a loan is assumable, they often include this information in the listing.

Some multiple listing service (MLS) systems also have a built-in field for “Assumable,” which allows you to select this specific filter when running a search.

If a site’s filter does not include an “Assumable” filter option, enter specific keywords like “Assumable mortgage,” “Assumable,” or “Assume.” This method can filter out listings that don’t meet your criteria, narrowing your search to properties with potential assumable loans.

When using major sites like Zillow, the keyword option is located under the “More” menu or the “Advanced Search” tool. You can also try including keywords related to loan types that you know are assumable, such as “VA loan,” “FHA loan,” or “USDA loan.” On some sites, loan-type information can be found in the “Mortgage History” section of a listing.

However, there will be other homes on the market with assumable loans that will not appear on a standard keyword search.

3. Use assumable loan websites and online services

There are modern websites and online services dedicated to finding home listings with assumable mortgages. These platforms are specifically designed to connect buyers with sellers offering assumable loans, making them a focused resource in your search. We discuss below some of the platforms worth exploring.

What is Roam (withroam.com)?

A real estate services startup called Roam makes the search for assumable mortgages even more convenient. The company specializes in identifying home listings with low-interest-rate assumable mortgages.

According to the company’s founder, Raunaq Singh, Roam is the first real estate service to provide a data feed exclusively made up of homes eligible for loan assumption. The company’s homepage highlights its services and claims homeowners can save over $100K.

Because Roam is a licensed real estate broker and a member of multiple listing services, the company has access to all the same listings a traditional real estate agent can view. The service cross-references mortgage data with public records to compare and locate homes for sale that are financed by assumable FHA or VA loans.

The cost to use Roam is 1% of the property’s purchase price. So on a home that sells for $400,000, you’ll pay $4,000, an amount you might make up in a matter of months from the money you can save on monthly payments with a low interest rate assumption.

Roam currently operates in more than 20 states, namely Arizona, California, Colorado, Florida, Georgia, Illinois, Indiana, Maine, Maryland, Massachusetts, Michigan, Missouri, Nevada, New Jersey, North Carolina, Ohio, Oklahoma, Pennsylvania, South Carolina, Tennessee, Texas, Utah, and Virginia.

Service fees and locations can change. Check Roam’s FAQ page for updates.

What is AssumeList (assumelist.com)?

AssumeList is a real estate search platform that provides homebuyers and agents the ability to find on- and off-market properties with assumable mortgages.

According to the website, all the listings on the platform “contain an interest rate below 5% and the vast majority have rates of 3% and lower,” allowing buyers to cut down thousands in monthly interest.

Veteran-owned and developed from the ground up, AssumeList is available in over 20 states, including Arizona, California, Colorado, Delaware, Florida, Georgia, Hawaii, Illinois, Maryland, Massachusetts, Michigan, Minnesota, Nevada, New Jersey, North Carolina, Pennsylvania, South Carolina, Texas, Tennessee, Utah, Virginia, Washington D.C., West Virginia, and Wisconsin.

AssumeList charges a monthly fee for access to its searchable database ($29 a month for homebuyers and $79 a month for licensed agents), which can be canceled at any time. Visit the company’s FAQ page for more information.

What is Assumable.io?

Assumable.io is a platform that provides access to over seven million assumable mortgage homes with rates below 4%. It operates in all 50 states and more than 6,500 cities, unlike other platforms that cover only limited markets.

Unlike other platforms, assumable.io does not charge buyers up to 1% of their transaction. It allows users to search and filter homes, making it easier to find options that meet their needs.

There are also specialized consulting and listing firms, such as Assumption Solutions, that help homebuyers, sellers, and their agents complete a successful mortgage assumption. For a fee, these companies will assist with the transfer process or help you find a listing with an assumable loan.

How does an assumable mortgage work?

When assuming a mortgage, the loan balance from the existing borrower is transferred to you, placing the responsibility of the remaining payments on your shoulders. Typically, this entails taking over the original terms set for the previous homeowner, such as the interest rate and monthly payment amounts.

The process is similar to getting a regular mortgage, but with some distinct steps. Here’s a general outline:

- Identify a home with an assumable mortgage: First, confirm if the home’s loan is assumable. Contact the homeowner’s lender for permission to assume the loan, a task often handled by a real estate agent if you’re working with one.

- Determine the remaining loan balance: Assess the remaining balance on the seller’s mortgage and see how much cash you’ll need for closing. If additional financing is necessary, explore lenders willing to provide it.

- Apply for the loan: Submit an application for the assumable loan. The process and criteria vary by lender, similar to a traditional mortgage application.

- Get lender approval: You’ll need to obtain approval from the existing lender and demonstrate your ability to assume the mortgage debt.

- Sign an assumption agreement: You’ll sign an assumption contract, officially transferring the mortgage debt responsibility to you.

- Finalize the sale: Complete the necessary paperwork to close the sale. This often includes signing a release that absolves the seller from the original loan’s obligations, a step that’s crucial in VA loan assumptions to prevent the veteran from losing future loan benefits.

- Make the loan payments: You will now start making mortgage payments following the existing terms, including the repayment period and interest rate.

Broesamle says you don’t need to walk the assumable mortgage path alone. An experienced agent can be your navigator. “I work with [clients] and our inside lender to make the process as easy as I can. I have them speak to the lender or give them a foreshadowing of events to expect during the process, and the things that they’re going to get […] to complete the process.”

What happens to the seller’s equity?

When a home has an assumable mortgage, the buyer usually takes over the existing loan but might still need to pay the seller the difference between the sale price and what’s left on the mortgage. This is called the seller’s equity, which reflects the property appreciation and the portion of the mortgage the current owner has already repaid.

If you don’t have enough cash to cover that gap, you might use a second loan or other financing to make it work. This setup lets the seller get their full equity while the buyer assumes the mortgage.

That said, as with any home purchase, you must plan your budget and know how much house you can afford. Whether you’re buying a home with a traditional mortgage or a mortgage assumption, you will need to compensate the seller for the equity they’ve built up in the home.

So for example, if you buy a $450,000 house from a seller who has an outstanding mortgage balance of $250,000, they have $200,000 worth of equity stake that belongs to them. You will need to pay the seller that $200,000 when you close the sale.

Pros and cons of assumable mortgages

Assumable mortgages can be a great way to snag a low-interest loan, but they’re not without their trade-offs. Like anything in real estate, there are benefits and some potential drawbacks to consider. Knowing the pros and cons can help you figure out if this option makes sense for your next home.

Pros of assumable mortgages

- Lower interest rate: Assumable mortgages often offer lower interest rates compared to current market rates, potentially leading to significant savings over the loan’s lifespan.

- Reduced out-of-pocket costs: Homes with low equity can mean less cash needed at closing, reducing initial expenses.

- No need to shop for mortgages: This process eliminates the need to compare lenders, streamlining the mortgage acquisition. Even if financing the seller’s equity is necessary, it’s often easier to qualify for this smaller, separate loan.

- Optional appraisal: While an independent appraisal is still advisable, it’s often not a requirement in a mortgage assumption, possibly saving time and money.

Cons of assumable mortgages

- Substantial cash required: If the seller has significant equity or the property’s value greatly exceeds the mortgage balance, you might need a considerable sum to cover their equity. Additionally, some lenders may be reluctant to finance a second mortgage.

- Limited availability: Assumable mortgages are less common, which can restrict your home-buying options.

- Challenging loan approval process: The approval process can be stringent, with lenders enforcing strict qualification criteria. Agency approval is often required for some government-insured loans.

While there are some challenges to navigate, Broesamle believes the pros can outweigh the cons for hopeful buyers feeling sidelined by high monthly mortgage payments.

“It’s a great value to take advantage of this with the high interest rates we have now,” he says. “Because if you can get the loan assumed, you know, you’re going to save yourself up to 50% in a rate […] If you can take advantage of that program, you’re going to save yourself a ton of money.”

Seller pros and cons

Offering an assumable mortgage can attract more buyers, especially in a high-interest market. Understanding the benefits and potential drawbacks helps you make an informed choice.

Pros

- Fast sale: If your interest rate is lower than what’s out there, buyers might jump at the chance to take over your loan.

- Competitive listing: Your home can be more appealing compared to others with higher-rate mortgages.

- Potentially higher price: A low-rate mortgage can let you list your home for a bit more.

Cons

- Approval needed: The buyer still has to get approved by the lender, which can slow things down.

- Smaller buyer pool: Only buyers who meet the lender’s requirements can assume the loan.

- Less cash upfront: If your loan balance is high, you might need to work out extra financing with the buyer.

If my loan is assumed, am I fully clear of the debt?

In the vast majority of cases, yes. When handled correctly and thoroughly, or with the help of a professional service, assuming a loan relieves the original borrower of the debt responsibility.

The proper process will include getting lender approval and submitting all required forms to release the seller from liability. In cases involving VA loans, getting the proper release forms completed is especially important to retain veteran loan entitlement benefits. The least complicated way to have your VA loan entitlement released is if your mortgage is assumed by another qualified military buyer.

Is it difficult to qualify for an assumable mortgage?

The qualification process for an assumable mortgage mirrors that of a traditional mortgage in many ways. Lenders evaluate factors such as your credit score, debt-to-income ratio (DTI), and overall financial health to determine your reliability as a borrower.

Necessary documentation typically includes proof of income, identification, and possibly your employment history. Fulfilling these criteria is essential for gaining lender approval, though the exact requirements may differ.

Seek advice from a mortgage professional to understand the process and find a suitable lender for your home-buying journey. Moreover, consider partnering with modern real estate solutions companies that can manage your loan assumption from start to finish.

How much does it cost to assume a home mortgage?

Assuming a mortgage incurs various expenses, similar to acquiring a new mortgage. These can include buyer’s agent’s commission, down payments, closing costs, and inspection fees.

A unique cost in this process is the assumption fee, which varies based on the lender’s policy, the investor behind the mortgage, and state regulations. This fee is typically a percentage of the unpaid principal or a fixed amount.

For VA loans, an additional VA funding fee, usually 0.5% of the loan balance, may apply. Exceptions exist, notably for VA disability beneficiaries, active-duty Purple Heart recipients, and surviving spouses eligible for Dependency and Indemnity Compensation (DIC). It’s advisable to consult with your lender for a detailed breakdown of the costs associated with mortgage assumption.

What are some pitfalls to watch for when assuming a mortgage?

Assuming a mortgage can seem like a shortcut to homeownership, but there are a few things you’ll want to keep an eye on. It’s not always as simple as taking over someone’s loan. Hidden fees and unexpected property issues can all cause headaches if you’re not careful. Before jumping in, it’s smart to know the risks.

Here are some common pitfalls to watch out for:

- Hidden costs: Just because you’re taking over someone else’s mortgage doesn’t mean you’re skipping fees. You might still be responsible for closing costs, title search fees, and other charges. These can add up quickly if you’re not prepared.

- Outdated loan terms: That older mortgage may have a higher interest rate than what’s available today. You could miss out on better deals by assuming an outdated loan. Always compare current market rates before deciding.

- Unpaid property issues: Assuming a mortgage doesn’t mean you’re clear of everything. Unpaid property taxes or liens can sneak up on you. It’s crucial to do a title search before signing anything.

- No release for the original borrower: In some cases, the seller might still be liable if you default. That can cause legal or financial trouble for both of you down the line. Make sure the assumption agreement includes a full release.

Can I assume a mortgage after someone’s death?

Mortgage assumption is an option when inheriting a home from a deceased family member. This is often feasible even in the absence of an assumption clause or for conventional loans. Typically, in cases of inheritance, the new borrower may not need to fulfill all standard qualification criteria if they were related to the deceased.

Can a mortgage be assumed post-divorce?

In a divorce scenario, if one spouse is granted full ownership of the property, they can usually assume the existing mortgage. The lender will assess their financial situation, including income, assets, and creditworthiness, to verify their ability to maintain the mortgage payments. Seeking guidance from a home loan expert is beneficial for smoothly managing the assumption process in such circumstances.

Should I consider assuming a mortgage?

Assuming a mortgage can be beneficial, especially if the home you are purchasing has a favorable interest rate, offering potential savings in time and money. However, this option has its own set of limitations and considerations.

HomeLight can connect you with a knowledgeable real estate agent in your area for guidance in finding properties with assumable mortgages. Additionally, consulting with a real estate attorney is recommended when exploring the possibility of an assumable mortgage.

While there are risks and challenges involved, assumable mortgages are a creative solution to rising borrowing costs. The hunt takes planning, patience, and effort, but you may walk away with a treasured home at an interest rate that eases the path to ownership.

Header Source: (Johnson Johnson / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.