How to Read An Appraisal Report: Skim for the Highlights, Page by Page

- Published on

- 8 min read

-

Emma Diehl, Contributing AuthorClose

Emma Diehl Contributing Author

Emma Diehl, Contributing AuthorClose

Emma Diehl Contributing AuthorEmma's work has been featured in Huffington Post, NPR and XOJane. When she's not combing her neighborhood for open houses, she's writing about technology, real estate or data.

-

Sam Dadofalza, Associate EditorClose

Sam Dadofalza Associate Editor

Sam Dadofalza, Associate EditorClose

Sam Dadofalza Associate EditorSam Dadofalza is an associate editor at HomeLight, where she crafts insightful stories to guide homebuyers and sellers through the intricacies of real estate transactions. She has previously contributed to digital marketing firms and online business publications, honing her skills in creating engaging and informative content.

You love your home, but let’s face it: its appraisal report is not a real page-turner. No judgment if your eyes start to glaze over halfway through the first section. However, it’s one of those documents that’ll be super useful to decipher if you ever decide to get your home professionally valued or if there’s a dispute over how much your home is worth when you sell it. Understanding how to read an appraisal report is key to making informed property decisions.

In a nutshell, this document contains the appraiser’s opinion of value and the factors the appraiser used to arrive at that number.

“I’d say 90% of the time, appraisers do a fantastic job,” says John Krol, an accomplished Naples-area real estate agent who completes 88% more sales than the average agent in his locale and regularly works with appraisers. But there’s a small chance that “the appraiser doesn’t have what they need or it’s due the next day,” explains Krol. That’s when some honest mistakes might occur.

Get an Estimate on Your Home's Value

Our Home Value Estimator uses your property information and local housing market data to deliver an accurate home value. You’ll receive a detailed analysis of your home straight to your inbox immediately, and if you’re looking to sell, we’ll help connect you with top agents in your area.

We spoke with Krol, consulted with two of the largest appraiser associations in America, and read over tedious appraisal reports to bring you this guide on how to skim one for the good stuff. You’ll know where to search for common errors on the Uniform Residential Appraisal Report, the most commonly used appraisal form totaling 7 pages.

First, obtain a copy of the appraisal report if you don’t have one

When you sell your home, you won’t automatically get a copy of the report, but you can request one and the lender will have to provide it to you in 30 days time. If the appraisal came in under the contract price, your real estate agent will be able to fill you in on the details right away. In the event that you get an appraisal outside of the home sale process, the appraiser should provide you with a copy of the report automatically.

Page 1: Check that your address looks correct

It’s easy to spot errors in this section, but it’s one a lot of homeowners will breeze right past. Focus your attention on page one at the top of the report under the “Subject” section. Confirm that the “Property Address” is accurate, including the ZIP code and County. If it’s incorrect, you might have the wrong report altogether.

Source: (Fannie Mae)

Source: (Fannie Mae)

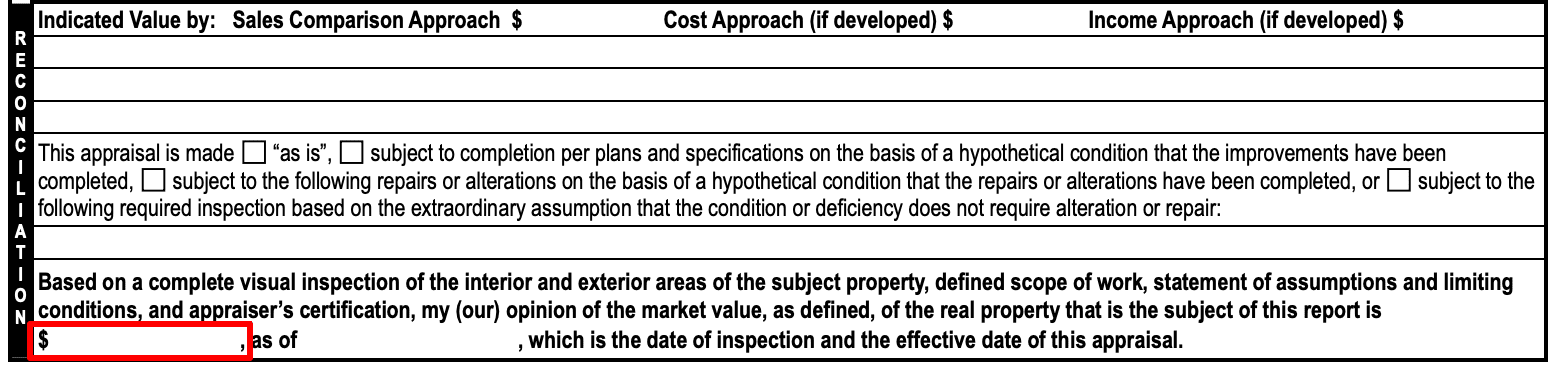

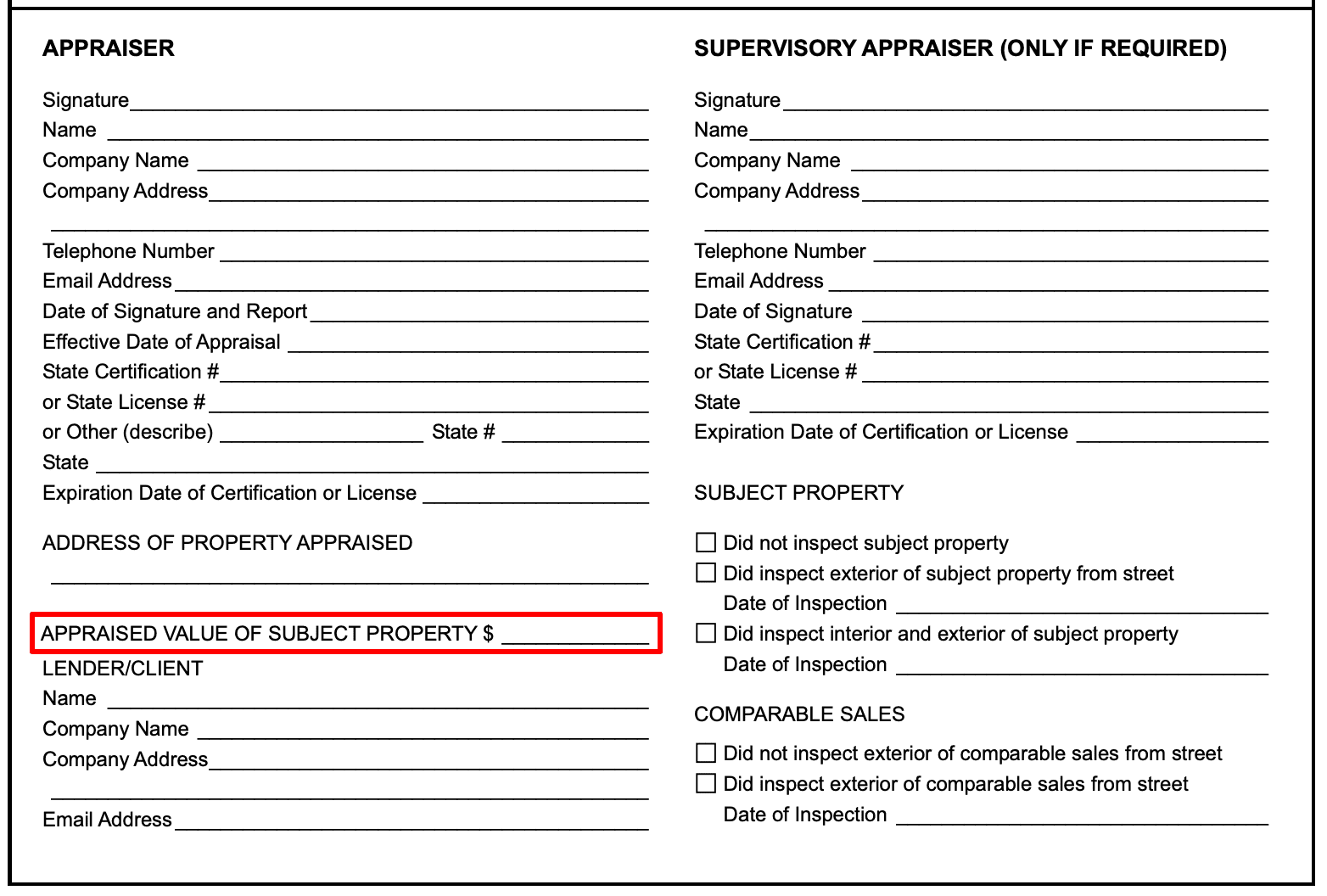

Pages 2 and 6: See what your home appraised for

Finding the total appraised value of your property is likely the main reason you’re reading this document, but the figure is surprisingly tricky to find.

Start on the second page. In the lower left-hand corner of the “Reconciliation Section,” you’ll find a fill-in-the-blank section that certifies the total appraisal value as of the date it was conducted.

Source: (Fannie Mae)

Source: (Fannie Mae)

The same total is on the sixth page, in the lower right-hand corner after the line reading: “APPRAISED VALUE OF SUBJECT PROPERTY.” Make sure these two totals match and confirm the date of the appraisal is correct.

Source: (Fannie Mae)

Source: (Fannie Mae)

That figure didn’t just fall out of the sky. Next, you’ll want to explore how your appraiser came to it.

Pages 2 and 3: Why is your home worth that much?

Diving deeper into the report, there are three approaches an appraiser can take to calculate the value of your property:

1. Comparable Sales (Page 2). Analyzing comparable sales is the most common approach professional appraisers use to figure out the value of your property. Taking up nearly the entire second page, the “Sales Comparison Approach” uses data from similar recent home sales in your area to determine the value of your property.

- Source: (Fannie Mae)

In these “comps” selected by the appraiser, you’ll want to pay attention to a few key points:

Date of Sale: How recent was the comparable property sold? Within the year? Longer? If you’re in a rapidly growing market, it’s important that the comp is as recent as possible, as it will reflect the rising rates in your market.

Comparability: The house needs to be similar to yours to be used as a tool of comparison. But only homes that have already sold can qualify as a comp. Make sure all three properties listed have actually sold, and aren’t just on the market. Otherwise, this is an inaccurate reflection of price.

Location: “If your house is on a private lane, and your appraiser used a comp that’s on a major highway, that’s a really poor location compared to yours,” says Krol. “That’s a common error.” A quick glance at Google Maps might tell you all you need to know about a comp’s location as compared to yours.

Cross-reference each of the above points with the actual sales record to ensure there’s no mistake in square footage and sales price. Then, take a look at the “Net Adjustment Total” line to see if the appraiser has adjusted the price of your property up or down based on each comp. If you have questions or if something looks off, loop in your real estate agent for a second opinion.

2. Cost Approach (Page 3). If your property is somehow unique, or new construction, your appraiser might choose to use the cost approach method to determine the value of your home. You’ll find the cost approach section on page 3, under “Cost Approach to Value”

Oftentimes, this method is used on high-end properties when comps just won’t cut it, or a unique property where comps simply don’t exist. It’s also used in instances where your home is under or over-improved for the area. So if you’re the best house or the “needs most improvement” house on the block, your appraiser might choose this method.

Source: (Fannie Mae)

Source: (Fannie Mae)

The cost approach is determined in two ways:

Reproduction: What would it cost to replicate this property? This takes into account the cost of original materials and the value of the lot itself. It also factors in property depreciation.

Replacement: What would it cost to recreate this property using new materials and methods of design? This assumes you’re not looking for original materials or methods, which might be out of vogue or no longer available. It will also factor in the cost of the lot.

The cost approach method is considered less reliable than comparable sales but is used when there are no comps available.

3. Income Approach (Page 3). Found below the “cost approach” section, the income approach is located under “Income Approach to Value” on page 3. This method should only be used if the seller generates income on the property through renting or leasing it.

Source: (Fannie Mae)

Source: (Fannie Mae)

The appraiser will take net income on the property, subtract expenses, and calculate the “capitalization rate” or Net Operating Income (NOI) to get an accurate read on the property’s worth.

When it comes to determining value, the appraiser is only required to use one of these methods. Take care to understand why the appraiser chose this method. This section is often best reviewed with your real estate agent, who will have a deeper understanding of comps in your market.

“Many sellers don’t realize the added value of someone who knows the business and is experienced with the valuation process,” says Krol. Don’t be afraid to ask your agent to look over the report, especially the comps, with you.

Page 1: Property description

Back on page 1, you’ll find the property description under the “Improvements” section. If this section is accurately completed, it’s a strong indicator that your appraiser knows the property well. While it starts on page one, depending on your appraiser, it might spill over into an appendix and include images and additional descriptions.

- Source: (Fannie Mae)

Pay close attention to the fill-in-the-blank sections, namely the General Description, Foundation, Exterior, and Interior, and check if the information are accurate. Below this portion, you’ll find “Additional Features,” where your appraiser should document any specialty appliances, including energy-efficient items or special amenities that add value to the property.

If you’ve recently renovated a portion of your home, it should be documented in the “Improvements” section. Similarly, if some items or features need repairs, they’ll be listed here. Be forewarned, this section can get a bit dry — the appraiser is objectively judging your property, breaking it down to square footage and building materials.

Continue to scan this section and read any comments the appraiser provides. Try to read it with an impartial eye, but if you find something that doesn’t sit right, bring it to your real estate agent for further discussion.

Page 6: Your appraiser’s onsite visit

On page 6, you’ll get a better sense of the legwork your appraiser did on the property. Under “SUBJECT PROPERTY” in the lower right-hand corner, the appraiser will indicate the steps they took to examine your property. That includes whether they visited your home, and inspected both the interior and exterior.

Source: (Fannie Mae)

Source: (Fannie Mae)

This section will also show whether the appraiser physically looked at the exterior of comparable homes in your area. If an appraiser didn’t get a chance to enter your property or check out the exterior, that might indicate a lack of familiarity with your property.

Page 1: Neighborhood Score

Finally, flip back to page one under the “Neighborhood” section. Here you’ll find data gathered around your property’s neighborhood.

- Source: (Fannie Mae)

Did the appraiser get the characteristics right? Are they accurately identifying trends?

If you’re selling in an up-and-coming neighborhood, pay particular attention to this section. If your appraiser is new to the area or unfamiliar with the geography, they might slip up here.

What to do if you find an issue with your report

“If you’re in the middle of a deal and you have an appraisal that you think is wrong, you could appeal,” Krol says. If it’s not a clear numerical error, talk it over with your agent to make sure it’s not based solely on emotion or frustration with the sales process.

Since the 2008 housing crisis, the appeal process has become a little more challenging, says Krol, and you won’t want to waste energy on an illegitimate appeal.

If you decide to appeal the appraisal, you’ll take the following steps:

- Contact the lender. Since the appraiser works for the lender, you’ll reach out to them and notify them of the error. Lenders each have their own process to address errors.

- Address the problems impartially. Don’t let emotions drive this appeal. Work with your agent to write out the issues with the appraisal report, whether it’s simply numerical errors or a larger issue.

- Start a second appraisal. If there’s a small error or two in the report, the appraiser will likely fix it and send over an updated report. However, larger issues will warrant a second appraisal, which should be conducted by a new appraiser, says the Appraisal Institute. You should also make sure the second appraiser is appropriately qualified with a national appraisal organization, such as the Appraisal Institute or the American Society of Appraisers.

- File complaint (if applicable). If you find a major issue with the appraiser, you can always file a complaint to your state appraisal board or professional organization.

Reading your home’s appraisal report can be tedious, but it will provide a rundown of your home’s value which is, in itself, kind of exciting. However, when in doubt, remember that becoming an appraiser calls for 150 hours of education so they’ve got a good handle on what goes into making one of these reports.

If you need assistance understanding the appraisal report or the overall process and want to maximize your sale price, work with an experienced real estate agent. Our Agent Match tool analyzes over 27 million real estate transactions and thousands of reviews to match you with a local top agent.

Price Your Home to Minimize the Chance of a Low Appraisal

Our Home Value Estimator is a great starting point, and we’ll send you a detailed analysis of your home’s value based on local housing market data.

Header Image Source: (Matthew Henry / Burst)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.